The Rebound Continues

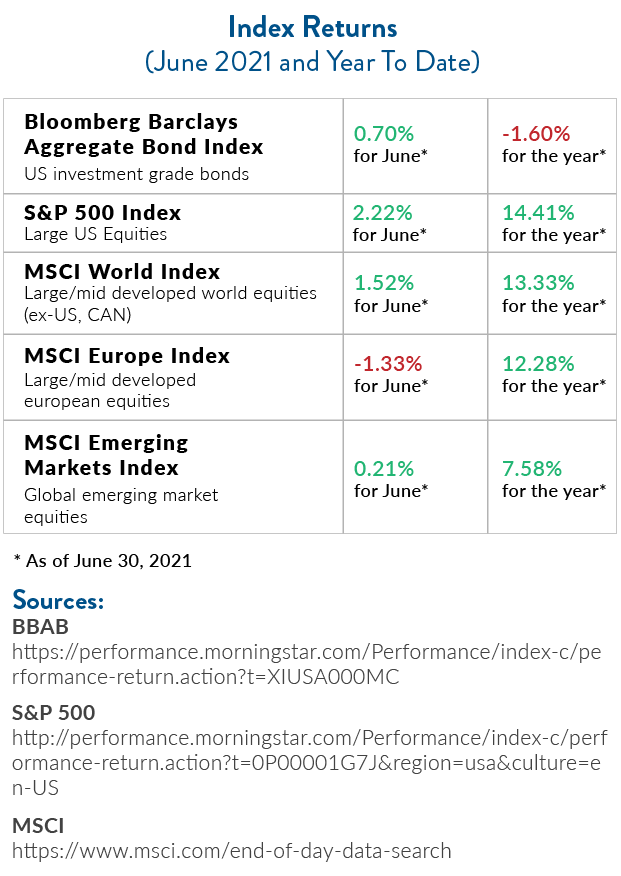

Markets reached new highs in the first half of this year, driven by a pandemic rebound and all the optimism that entails. Year-to-date returns for the S&P 500 are 14.41% through June 30, the 18th best start to a year for stocks.[1]

All said, businesses are doing well in the pandemic rebound.[2] S&P 500 companies are expected to post earnings-per-share growth of almost 63% for the second quarter, compared to the second quarter of 2020.

All said, businesses are doing well in the pandemic rebound.[2] S&P 500 companies are expected to post earnings-per-share growth of almost 63% for the second quarter, compared to the second quarter of 2020.

Obviously, the same period last year was marked by broad economic shutdowns, but this does go to show that a recovery seems to be taking hold, at least in the U.S. In this note, we’ll cover more about the economy and what might lie ahead.

Jobs Are Coming Back—But Staying Unfilled

Employment is an interesting area right now—one that not only helps illustrate some of the complexities of the pandemic, but which directly impacts many of our business owner clients.

The unemployment rate is at 5.9% and we’re still down about 7 million jobs since the onset of the pandemic. This May, about 9 million Americans said they wanted a job but couldn’t find one. At the same time, job openings are at record highs, with 9.2 million positions available (again, as of May).

Why the disconnect?

There’s likely some level of skills or location mismatch between open jobs and job seekers, and in some cases workers are preferring to maintain remote work rather than returning to the office. In other cases, extended unemployment benefits have given workers more flexibility to be selective in their job search.[3] There are also those who’ve stayed out of the workforce in order to care for children and/or aging parents.

It’s also important to note that there are about 2.6 million workers who have retired since the pandemic, about 1.5 million more than would normally be expected.[4] Taken together, these factors could be helping to drive a complicated jobs recovery—one which still has more than a few knots to unravel.

It’s also important to note that there are about 2.6 million workers who have retired since the pandemic, about 1.5 million more than would normally be expected.[4] Taken together, these factors could be helping to drive a complicated jobs recovery—one which still has more than a few knots to unravel.

Of course, with school starting in the fall and federal unemployment supplements ending, we could see a more rapid return to “business as usual” later this year. While the employment situation isn’t something we’re concerned about, it does drive home the point that the recovery isn’t necessarily going to be complete, immediate, and without the occasional bump in the road. This has become obvious as the indoor mask mandate returns to Los Angeles County starting Sunday, July 18 – and it’s impossible to predict the economic impact of the Delta strain.

What About Inflation?

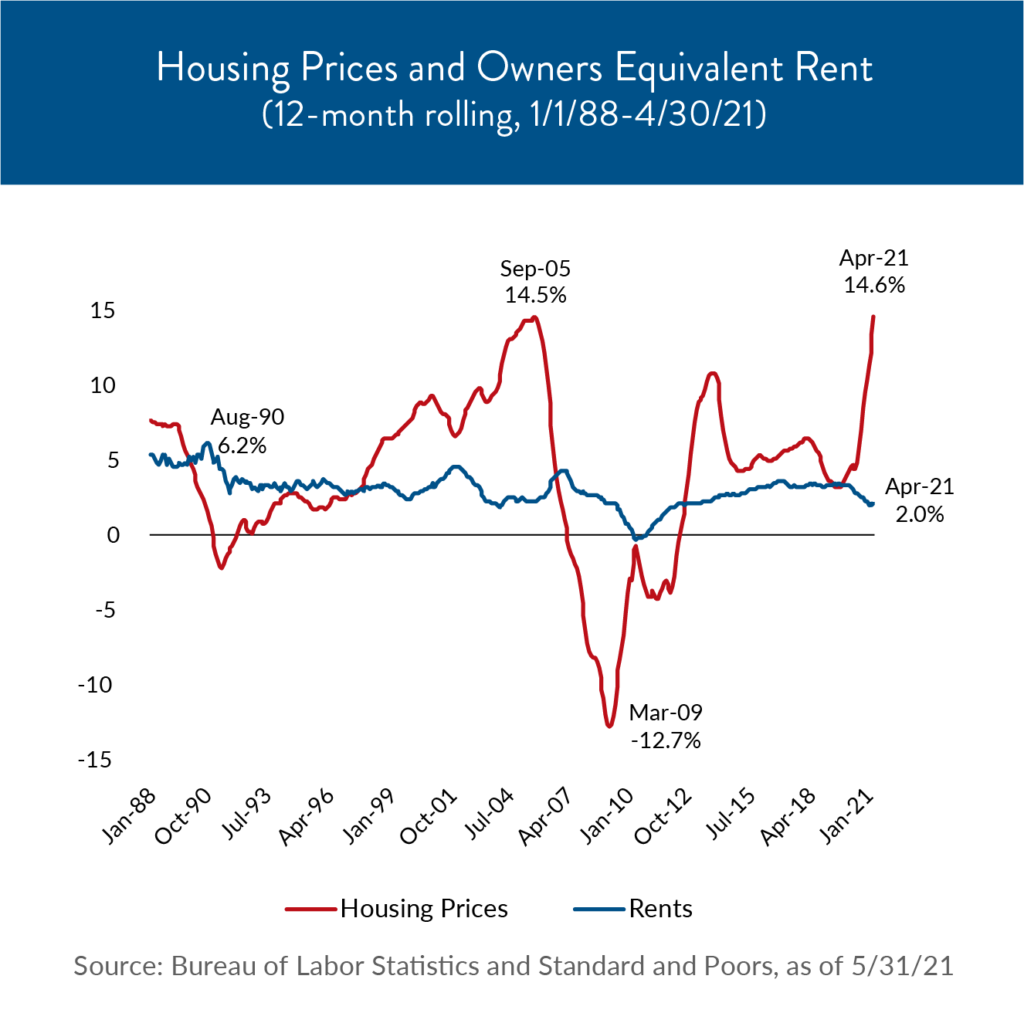

Another interesting bump in the road has been inflation. If you’ve filled your gas tank or looked at buying property recently, you’ve probably noticed an immense increase in prices from a year ago. Gas prices are up 40% for the year, reaching their highest level in seven years.[5] Home prices have jumped so fast this year that we’ve hit the largest-ever difference between home price inflation and rent growth.[6]

While these types of data points are, in large part, driven by the tumult of a rapid recovery, we could be seeing some inflation trends that persist into the future.

The Federal Reserve revealed two new rate hike projections for 2023 and higher inflation projections for 2021.[7] Recent inflation measures have exceeded the 2% average annual target, though the Fed has continued to reiterate that it will need to see sustained progress beyond the immediate recovery period before making any policy changes.

That said, even an average 2% annual inflation rate will be a change of pace. A Wall Street Journal survey of economists found an average forecasted rise in inflation of about 2.3% annually in 2022 and 2023—higher than we’ve seen since 1993.[8] While this is not a bad thing, a slightly higher average inflation rate could have an impact on everything from borrowing to portfolios, making it an important data point to monitor going forward.

That said, even an average 2% annual inflation rate will be a change of pace. A Wall Street Journal survey of economists found an average forecasted rise in inflation of about 2.3% annually in 2022 and 2023—higher than we’ve seen since 1993.[8] While this is not a bad thing, a slightly higher average inflation rate could have an impact on everything from borrowing to portfolios, making it an important data point to monitor going forward.

Continuing to Adapt

Whether we’re adapting to a new regime in inflation, confronting new and future challenges from the ongoing pandemic, or navigating a recovering labor market, there’s a balance to be made between long-term strategic thinking and short-term adaptation. We do think there will be some necessary changes in strategies over the coming years based on shifting economic conditions, but we caution—as always—against rash or emotional decision-making.

Of course, right now that can be difficult (especially if you want to buy a house). With so much pent-up demand and pandemic-related complexities, there’s a bit of noise in the economic data. This doesn’t make the data wrong, it just means it’s a good idea to exercise caution and prudence before taking next steps.

As always, please don’t hesitate to reach out to us with your questions, thoughts, or concerns. We’re here to help. And in the meantime, we hope you’re enjoying a wonderful summer with friends, family, and loved ones.

Download print version of this article.

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of Mid Atlantic Capital Corporation (MACC). Neither JSF Financial LLC nor MACC gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase or sale of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or MACC as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Europe Index captures large and mid-cap representation across 15 developed markets countries in Europe and covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 emerging markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

Sources:

[1] Source: https://www.blackrock.com/us/individual/literature/investor-education/student-of-the-market.pdf

[2] This section: https://www.ft.com/content/9aeaa9a3-a27f-4923-b7ed-0079b9d7ce0b

[3] Source: https://www.wsj.com/articles/job-openings-are-at-record-highs-why-arent-unemployed-americans-filling-them-11625823021?mod=hp_major_pos3#cxrecs_s

[4] Source: https://www.bloomberg.com/opinion/articles/2021-07-09/labor-market-is-it-loose-or-tight-it-s-both?sref=c4RUGNV1

[5] Source: https://www.cbsnews.com/news/gas-prices-highest-in-7-years/

[6] Source: https://www.blackrock.com/us/individual/literature/investor-education/student-of-the-market.pdf

[7] This section: https://www.nasdaq.com/articles/june-second-quarter-2021-review-and-outlook-2021-07-01

[8] Source: https://www.wsj.com/articles/higher-inflation-is-here-to-stay-for-years-economists-forecast-11626008400?mod=trending_now_news_pos4

Performance table sources:

BBAB: https://performance.morningstar.com/Performance/index-c/performance-return.action?t=XIUSA000MC