Display results

10 March

Only Game in Town

March 2023 Market Update

In his 2016 book, Chief Economic Advisor at Allianz Mohamed El-Erian pointed out that central bank policy has been “the only game in town” since the 2008 financial crisis.[2] Monetary policy has been even more of a focus since the Federal Reserve (Fed) embarked on its rate hike campaign last year.

The Federal Reserve kicked off February with a widely expected 25 bps interest rate hike, raising rates to a target federal funds rate of 4.5-4.75%, its highest levels since 2007.[3]

As we discussed last month, markets seemed to be ignoring central bank warnings that interest rates would have to stay elevated. Despite Fed chair Jerome Powell explicitly saying at the beginning of February, “I just don’t see us cutting rates this year,” traders still expected the Fed to cut rates twice by year-end.[4]

However, economic data released subsequently increased expectations that the Fed would need to hold interest rates higher for longer.[5] Datapoints included:

– Core monthly personal consumption expenditures (the Fed’s preferred measure of inflation) increased 0.6% month on month in January and 4.7% year on year, compared to forecasts of a 4.3% increase[6]

– Headline inflation rose by 0.6% and 5.4% respectively[7]

– Employers added 517,000 jobs in January, compared to expectations of 187,000, and the unemployment rate edged lower to 3.4%, a 53-year low[8]

Markets Starting to Believe the Fed

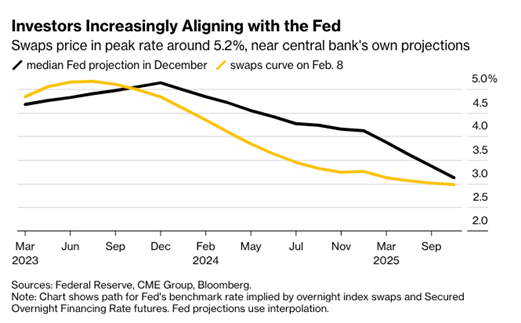

In response to the data, the markets are finally starting to reflect the Fed’s forecasted hawkishness. Markets now estimate the benchmark federal funds rate to land between 5.25-5.5% by July, which is more than 50bps higher than they expected to February.[9] Investors are now aligned with the last set of Fed interest rate projections published in December.[10]

PIMCO notes that eventually, these higher rates will slow aggregate demand and cool inflation, although monetary policy operates with an expected lag of anywhere between 12 and 24 months. Given that delay in impact, we’re likely to see more evidence of a slowdown in demand by midyear, which is also when yields are expected to peak.[11]

A peak level of interest rates is likely not sustainable for very long, which is why the market still believes that rate cuts are coming. In our opinion, we don’t need a recession for rates to be cut again — inflation just needs to be on a steady downtrend toward the target 2% level.

February Markets

As markets increased their interest rate expectations, bond yields increased (prices fell). Two-year Treasuries, a proxy for short-term rates, rose to its highest point since 2007,[12] causing a deep inversion of the yield curve between two and 10-year Treasuries. The “inversion” refers to the two-year yield trading higher than the 10-year yield, which is often viewed as a sign of an upcoming recession.

As the optimism from January faded, most assets, from stocks to bonds and commodities, fell.[13] Equity benchmarks ended the month lower with the S&P 500 down 2.6%, though still up for the year after January’s 6% rise.[14]

One Year In

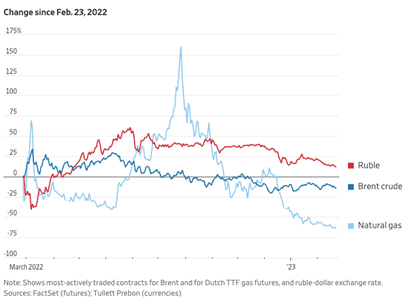

Sadly, this past month marked the one-year anniversary of the Russian invasion of Ukraine. The US and its allies issued fresh sanctions against Russia, but China’s financial system is still offering a lifeline for the Russian economy.[15]

Overall, many investors believe the war has made global inflation more entrenched, as it disrupts commodity markets, fragments supply chains, and encourages more spending on defense and energy.[16]

Source: https://www.wsj.com/articles/how-russias-invasion-of-ukraine-changed-financial-markets-5a80f469

However, some energy prices have settled around pre-invasion levels. Despite heavily traded Brent crude oil contracts spiking in price the weeks after the invasion, they’ve come back down.[17] That’s even with Western countries no longer buying Russian oil (benefiting US energy producers).[18]

America has stepped in to become the world’s largest exporter of liquefied natural gas, and natural gas prices have also fallen nationwide.[19] Unfortunately the outlier has been California, where we’ve faced unusually high gas bills due to low supply and unusually high demand, though those prices peaked in December.[20] We should be seeing a peak in our gas bills shortly!

In other areas, we’re still feeling the squeeze from stubbornly high food inflation, especially in grains, meat, and eggs.[21] Other factors are also at play here, in addition to the war.

Lingering inflation explains why the Fed has had to embark on such an aggressive tightening campaign. While businesses and markets may feel the heat from rising interest rates, ultimately the goal is to tamp down inflation and slow down economic growth.

What’s Next

The Fed meets again March 21-22, where they will be releasing their newest set interest rate projections, now that markets have finally caught up with December estimates.[22],[23] We’re likely to see another rate hike in March, but the Fed may have enough data on hand to signal a pause.[24]

As we set our clocks ahead and spring forward, it appears that the Fed still has a hold on the market narrative. With more clarity around the timeline of hikes, markets will likely turn more attention to earnings and the broader economy. Goldman Sachs CEO David Solomon has said the chance of a softer economic landing has improved from six to nine months ago, as inflation moderates.[25]

While questions continue to swirl about the economy and the impact of interest rates, our favored approach for long-term investors is maintaining a broadly diversified portfolio. This strategy focuses on a mix of investments carefully tailored to the risk profiles and goals of each investor. Please keep us informed of any changes in your financial situation or objectives so that we can help you address them!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

Sources:

[1] https://finance.yahoo.com/news/bulls-hit-asset-downdraft-reversing-211054902.html

[2] Book: The Only Game in Town: Central Banks, Instability, and Recovering from Another Collapse by Mohamed A. El-Arian. June 2, 2017, Yale University Press

[3] https://www.cnbc.com/2023/02/01/fed-rate-decision-february-2023-quarter-point-hike.html

[4] https://www.reuters.com/markets/global-markets-central-banks-analysis-pix-2023-02-02/

[5] https://www.ft.com/content/f74f14b4-5de1-4ef6-aa18-b4c0d7cedb69

[6] https://www.cnbc.com/2023/02/24/key-fed-inflation-measure-rose-0point6percent-in-january-more-than-expected.html

[7] https://www.cnbc.com/2023/02/24/key-fed-inflation-measure-rose-0point6percent-in-january-more-than-expected.html

[8]https://www.cnbc.com/2023/02/03/jobs-report-january-2023-.html

[9] https://www.ft.com/content/f74f14b4-5de1-4ef6-aa18-b4c0d7cedb69

[10] https://www.bloomberg.com/news/articles/2023-02-08/big-bet-on-hawkish-fed-seeks-135-million-gain-on-6-policy-rate

[11] https://www.pimco.com/en-us/insights/blog/data-alters-markets-expectations-for-peak-policy-rate-but-not-outlook-for-fed-cuts

[12] https://www.ft.com/content/da541c73-db3b-4f05-983a-fbc800d30be3

[13] https://finance.yahoo.com/news/bulls-hit-asset-downdraft-reversing-211054902.html

[14] https://www.wsj.com/livecoverage/stock-market-news-today-02-28-2023

[15] https://www.wsj.com/articles/west-starts-issuing-fresh-sanctions-against-russia-93c6b752

[16] https://www.wsj.com/articles/russia-ukraine-war-impact-on-the-world-4f318a37

[17] https://www.wsj.com/articles/how-russias-invasion-of-ukraine-changed-financial-markets-5a80f469

[18] https://www.wsj.com/articles/russia-ukraine-war-impact-on-the-world-4f318a37

[19] https://www.wsj.com/articles/russia-ukraine-war-impact-on-the-world-4f318a37

[20] https://www.nytimes.com/2023/02/16/us/california-natural-gas-prices.html

[21] https://www.pimco.be/en-be/insights/blog/fed-seeks-to-balance-competing-risks

[22] https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

[23] https://www.bloomberg.com/news/articles/2023-02-08/big-bet-on-hawkish-fed-seeks-135-million-gain-on-6-policy-rate

[24] https://www.pimco.be/en-be/insights/blog/fed-seeks-to-balance-competing-risks/

[25] https://www.cnbc.com/2023/02/14/goldman-sachs-ceo-david-solomon-on-soft-landing-odds-for-us-economy-.html

Read more