Display results

30 November

Tax Moves to Consider in Light of 2022’s Economic Challenges

Despite the roller coaster ride that has been 2022, there is still time to reduce this year’s tax burden. By planning and acting on the following tax moves now, you can stay ahead of the curve.

Consider a Roth IRA conversion or “Backdoor Roth”

Contribution limits apply to Roth IRAs based on modified adjusted gross income, which start kicking in when single filers earn over $129,000 and married filers make over $204,000.[i]

However, you can convert a traditional IRA to a Roth IRA by paying current income tax rates on the amount converted.[ii] Since this conversion can be done regardless of adjusted gross income, it is known as a “Backdoor Roth.” The major perk of this strategy is that in the future, all withdrawals from your Roth (that meet the appropriate withdrawal requirements) are tax-free. By contrast, withdrawals from your traditional IRA are fully taxed as income.

Further, if stocks and bonds are depressed you may indeed be converting at an opportune time since the future appreciation is tax free.

Revisit Your Estate Tax Exemptions—and Gifts

If you’re on track to reach the lifetime $12,060,000 per-person gift tax exemption in 2022,[iii] now’s a great time to use it. Even if Congress doesn’t lower the limit next year, the exemption expires at the end of 2025 anyway.

You can also transfer annual tax-free gifts to your loved ones. Typically, you can give up to $16,000 per person, per year with no tax consequences.[iv] A married couple can gift their married adult child and spouse a combined $64,000 a year, tax free.[v] In addition, one can also pay tuition directly to a school/university as well as pay direct medical expenses, which are excluded from annual and lifetime gift thresholds.[vi]

Gifts of Depressed Assets

Recent depressed asset values provide a unique opportunity to transfer substantial wealth now which will benefit family members for several future generations. Using a portion of your federal exemption to transfer current low asset values should be viewed as an opportunity. Depressed stock and business values can be considered a “natural discount” taken alone. When considered in combination with valuation discounts available from various wealth transfer strategies the “double” discount makes this a particularly attractive time to make gifts with property that is expected to appreciate during a market recovery.[vii]

Maximize Charitable Contributions

The IRS lets you claim a standard deduction or itemize deductions when filing your tax return. For 2022, the standard deduction for an individual is $12,950, and a married couple who files jointly can deduct $25,900.[viii]

However, if your allowable deductions, including charitable giving, are greater than these limits, you can realize a greater tax benefit by itemizing deductions. A bump in your 2022 charitable donation could put you above the threshold to itemize and give you a bigger tax break.

Donor Advised Funds

A donor-advised fund is essentially an investment account for charitable contributions. Making contributions of appreciated securities or cash can give you an income-tax deduction while making it easier to support causes or charities for the long-run. Once your contribution is made, you can take an immediate income-tax deduction. That’s why this is a useful strategy to consider before the end of the year. Your donation grows, tax-free, until you’re ready to contribute it to a cause. You can support any qualifying public charity with your funds.[ix]

Harvest Tax Losses

Given the extent of the market volatility in 2022, you may be straining to find some good news. Tax loss selling, also known as tax loss harvesting, can be used to reduce taxes on other capital gains. You can sell stocks and mutual funds to realize losses and then use those losses to offset any taxable capital gains you have realized during the year. Capital losses offset capital gains dollar for dollar and if your losses are more than your gains, you can use up to $3,000 of excess loss to wipe out other income.[x]

If you have more than $3,000 in excess loss, it can be carried over year to year for as long as you live. It can be tempting to move in and out of positions, but the wash-sale rule doesn’t permit you to write off losses if you sell and rebuy the same or similar security within 30 days.[xi]

The Remote Workplace

Since the coronavirus pandemic began nearly two years ago, an unprecedented number of people have started working from home. Remote work can trigger tax implications for both business and their employees that most people fail to think about. One of those implications is that you might be subject to double taxation if it is unclear as to where you actually reside and multiple states are vying for the right to tax your income.

To avoid these tax issues, it’s good to notify both your employer about your whereabouts. You should also consider documenting the dates of your travel, or if applicable, your move. If the move is a permanent one, take steps to establish your state of residence like changing your mailing address and getting a new driver’s license as soon as possible.[xii]

Conclusion

The right year-end tax moves for 2022 vary widely based on your personal financial situation and any planning moves you’ve already executed throughout the year.

These are just a few strategies that may be applicable to you—for specific ideas, it’s important to work with us and your accountant to figure out the most appropriate way forward. We’re here to help you quarterback that process and strategize specifics. While you’re likely to have heard from us already about year-end planning, please don’t hesitate to reach out if you have any outstanding questions about your tax situation.

Thank you for your ongoing support and trust throughout the year and we look forward to continuing working closely together with you in 2023.

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing. Consult your own tax adviser prior to engaging in any transaction.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[i] https://www.irs.gov/retirement-plans/plan-participant-employee/amount-of-roth-ira-contributions-that-you-can-make-for-2022

[ii] https://www.fidelity.com/tax-information/tax-topics/roth-conversion

[iii] https://www.irs.gov/businesses/small-businesses-self-employed/whats-new-estate-and-gift-tax

[iv] https://turbotax.intuit.com/tax-tips/estates/the-gift-tax/L1sFpFeXV

[v] https://www.elderlawanswers.com/will-you-owe-a-gift-tax-this-year-6069

[vi] https://www.actec.org/estate-planning/gift-tax-medical-expenses-tuition-payments/

[vii] https://www.hollandhart.com/depressed-asset-values-provide-unique-opportunity-for-wealth-transfer-planning

[viii] https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-2022

[ix] https://www.fidelitycharitable.org/guidance/philanthropy/what-is-a-donor-advised-fund.html

[x] https://www.fidelity.com/viewpoints/personal-finance/tax-loss-harvesting

[xi] https://www.investopedia.com/terms/w/washsalerule.asp

[xii] https://www.thezebra.com/resources/personal-finance/double-taxation-remote-work/

Read more

8 November

Back on the Seesaw

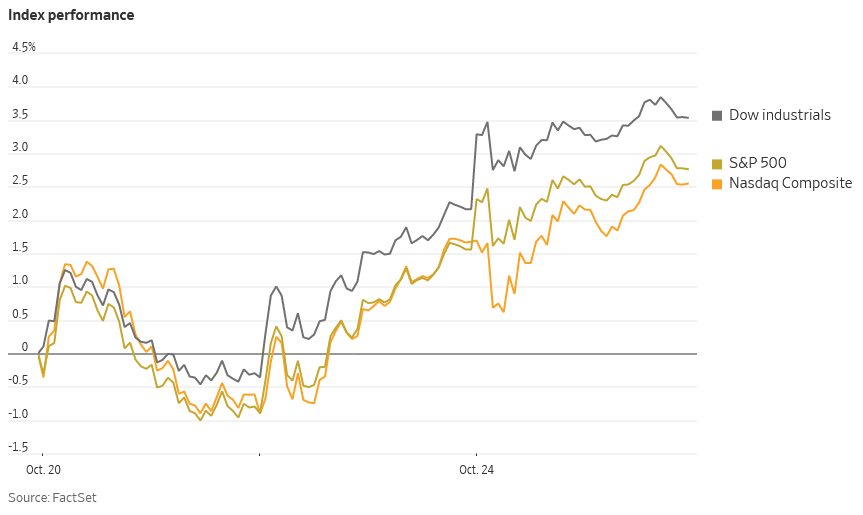

Quick Take: Equity markets bounced back from a two-month losing streak in response to 3rd quarter earnings and reports that the Fed could reduce interest rate hikes.[1]

As the holiday season approaches, equity markets made a brief comeback as the S&P 500 index climbed 8% in October, the first monthly rise since July.[2] The Dow Jones Industrial index posted its best month since 1976.[3]

Even though major tech earnings disappointed investors, the tech-heavy Nasdaq also rose 3.9%.[4] Investors responded positively to earnings results and reports that Fed officials may consider shifting to smaller interest-rate hikes of 0.5% starting in December.[5]

Source: https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

Economy Watch

Notably for recession watchers, US gross domestic product (GDP) grew again in the 3rd quarter by 0.6%, after two quarters of decline. Key components of this broad measure of US activity showed signs of a slowdown, as the Fed tries to rein in inflation with restrictive rate hikes.[6]

Given the rebound in 3rd quarter GDP and a strong jobs market, we haven’t yet reached recession territory. However, 98% of CEOs surveyed by The Conference Board are preparing for a recession, and even the most bullish outlooks are assuming an upcoming recession.[7] Bloomberg economists expect a recession within the next year.

Rate hikes have driven US Treasury yields near their highest levels (lowest prices) of the past decade, with the 10-year Treasury yield trading above 4.2%.[8] These high yields could unearth opportunities in government bonds and even Treasury bills.

Wait and See

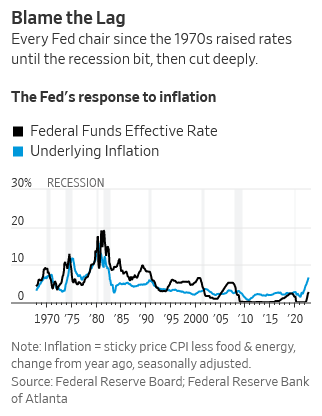

While markets tend to be forward-looking, the impact of interest rate hikes can have a considerable lag. After all, interest rate changes take time to filter through the economy. As borrowing costs rise and asset prices decline, consumer demand needs to slow to lower sales, so that companies can no longer raise prices.

Individuals and businesses may choose to slow the pace of borrowing and investing, but the lower demand that leads to businesses trimming their workforce is a multilevel process. Participants at the Federal Reserve’s (“the Fed”) September policy meeting noted that a significant portion of economic activity has still not had much of a response to higher interest rates.[9]

Source: https://www.wsj.com/articles/higher-interest-rates-can-take-a-long-time-to-bring-down-inflation-11666517405?mod=Searchresults_pos12&page=1

After months of rapid rate hikes, investors are hopeful that the Fed is nearing a pause or at least slowdown in interest rate hikes.

The market’s optimism over a potential turn in the rate hiking cycle has precedence. Looking back in history, every Fed chair since the 1970s has raised rates until a recession began, then pivoted to cut rates deeply.[10]

Continued high inflation and low unemployment could dash such hopes and pressure the Fed to press ahead with the hawkish policy to curtail inflation.

Earnings and a Bear Market Rally?

3rd quarter corporate earnings have been a mixed bag, with 35% of S&P 500 companies missing earnings.[11] Markets rallied as several corporate leaders expressed confidence in the strength of the consumer.[12]

Source: https://www.ft.com/content/af7de03e-8c68-41f5-ad79-1b82f4808482

While the US economy looks somewhat resilient, the reality is that we are seeing weaker growth and declining net profit margins in the S&P 500 companies. [13] Morgan Stanley Wealth Management Chief Investment Officer Lisa Shalett noted a disconnect between a lack of explicitly lower guidance during earnings calls and low levels of CEO confidence.[14] As a result, earnings estimates could still have room to fall.

Morgan Stanley strategist Mike Wilson, who until recently was a prominent stock market bear who predicted this year’s slump in equities, believes the October stock rally could have legs until the next earnings estimates pull back more meaningfully.[15] His view is that as markets transition to expect falling inflation and lower interest rates, stocks could grind higher in a bear market rally.[16] Of course, the timing of falling inflation and lower rates, along with the direction of the stock market, is still a major question mark.

Looking Ahead

Source: https://www.jpmorgan.com/wealth-management/wealth-partners/insights/midterm-elections-preview-potential-outcomes-and-market-implications

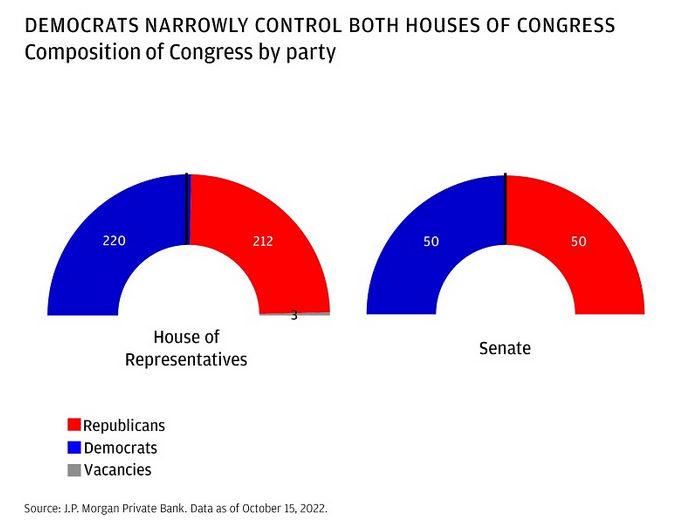

November brings the midterm elections, where analysts expect an uphill climb for Democrats. The consensus expectation for Democrats to lose seats in Congress could result in more gridlock, which historically tends to be positive for stocks.[17] Whether politics will have an impact against the tide of rising rates remains to be seen.

We’ll close out the year with one more Fed meeting in December. In November, the Fed, as widely expected, raised rates by 0.75% for the fourth consecutive time.[18] Investors parsed Fed minutes and Chairman Powell’s testimony, which indicates additional rate increases are on the horizon.

The October bounce back is another reminder of the unpredictability of markets and how quickly sentiment shifts. Most decisions based on short-term emotional views tend to be damaging to long-term performance. The bumpy ride underscores the benefits of a carefully pre-planned investing approach. Our experience through other “unprecedented times” has shown that long term investors are generally rewarded for staying the course.

Please reach out to schedule your year-end review or discuss any thoughts, concerns, or changes in objectives. We are blessed to live in a resilient country and look forward to honoring our great democracy by voting this week!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] https://www.cnbc.com/2022/10/30/stock-market-news-futures-open-to-close.html

[2] https://www.ft.com/content/af7de03e-8c68-41f5-ad79-1b82f4808482

[3] https://www.cnbc.com/2022/10/30/stock-market-news-futures-open-to-close.html

[4] https://www.ft.com/content/af7de03e-8c68-41f5-ad79-1b82f4808482

[5] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

[6] https://www.nytimes.com/2022/10/27/business/economy/us-economy-gdp.html

[7] https://www.morganstanley.com/ideas/q3-earnings-better-than-expected-how-long

[8] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-21-2022-11666349021

[9] https://www.wsj.com/articles/higher-interest-rates-can-take-a-long-time-to-bring-down-inflation-11666517405?mod=Searchresults_pos12&page=1

[10] https://www.wsj.com/articles/higher-interest-rates-can-take-a-long-time-to-bring-down-inflation-11666517405

[11] https://www.gsam.com/content/gsam/us/en/advisors/market-insights/market-strategy/global-market-monitor/2022/market_monitor_102822.html

[12] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

[13] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

[14] https://www.morganstanley.com/ideas/q3-earnings-better-than-expected-how-long

[15] https://news.yahoo.com/morgan-stanley-wilson-says-end-091001300.html

[16] https://www.bnnbloomberg.ca/morgan-stanley-s-wilson-says-bear-market-may-end-in-early-2023-1.1837567

[17] https://www.nytimes.com/2022/10/28/business/midterm-election-stock-market.html

[18] https://www.blackrock.com/us/individual/insights/blackrock-investment-institute/weekly-commentary

Read more