Stocks Lead the Way

Quick Take: Stocks continue to gain steam as optimism reaches highs relative to bonds.

As the scorching heat produced the hottest month on record, the S&P 500 notched a fifth consecutive positive month, up 3.1%.[1][2] Despite talk of 2023 being the “year of the bond,” bulls have so far created a flood of demand for the stock market.[3] Year-to-date, the S&P has climbed more than 19%, which is less than 5% away from the all-time high reached in January 2022.[4]

Year of the Stocks (so far)

Not many people saw this year’s rally coming. Wall Street strategists have had to revise bearish outlooks in recent weeks and update year-end S&P forecasts higher.[5] More than half of JPMorgan clients surveyed are now convinced that the US economy can continue to expand despite Fed tightening, which could explain the accompanying jump in plans to boost equity exposure. Already, stock exposure, as tracked by the National Association of Active Investment Managers, is at its highest levels since November 2021.[6]

Source: https://www.bloomberg.com/news/articles/2023-07-29/stocks-crush-year-of-bond-in-biggest-market-sentiment-shift-since-99

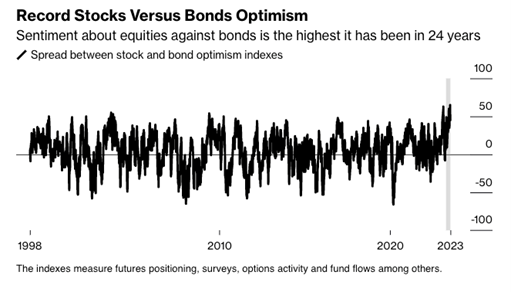

According to SentimenTrader models, investors are more optimistic about stocks relative to bonds than they have been in 24 years.[7] The fund flows reflect that sentiment – exchange-traded funds have seen a strong preference for equities over fixed income the last three months, which is a notable reversal from the beginning of the year.[8]

The shift has come from signs of slower inflation combined with strong economic data. Inflation continued to cool in June even as consumer spending rose, reflecting sustained economic momentum.[9] With the Fed potentially closer to ending interest rate hikes, the dollar is also falling, which could provide support to corporate profits.[10]

So where does the stock outperformance leave bonds?

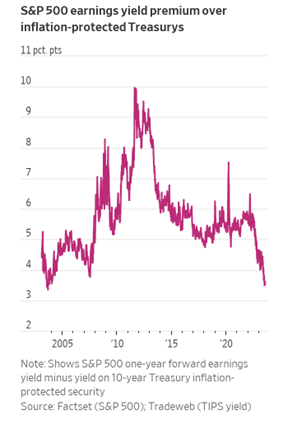

Given the strength in stocks, the additional reward for holding stocks over bonds has dropped to its lowest level in 20 years.[11] This equity “risk-premium” can be measured by the difference between the S&P 500 earnings yield and the yield on the 10-year US Treasury inflation-protected bond.

Source: https://www.wsj.com/articles/the-benefit-of-owning-stocks-over-bonds-keeps-shrinking-20528203

Bond bulls would argue that at high interest rates, bond coupon payments provide attractive low-risk income. Further, as the Fed seemingly approaches the end of this interest rate hike cycle, bond yields could head lower (prices higher). As inflation comes down and markets anticipate rate cuts in 2024, bonds could begin to outperform.[12]

Of course, bond markets can be driven by other factors, and we would be remiss if we didn’t touch on recent events in Japan. The Bank of Japan has historically anchored its interest rates to “rock-bottom” levels through a quantitative easing program used to stimulate the economy.[13] As a result, Japanese investors have spent more than $3 trillion investing offshore in search of higher yields.[14]

At the end of July, the Bank of Japan surprised the market by loosening its grip on yields in what could be a significant shift for global financial markets.[15] Even slight shifts in policy away from easy money could potentially bring some offshore money back to Japan and also drive up rates globally.[16]

In Pursuit of a Soft landing

Back in the US, the Fed hiked interest rates by another 25 bps in July, as anticipated.[17] After increasing 11 times from near zero rates in March 2022, the federal funds target rate is now 5.25-5%.[18] The fed funds rate guides borrowing costs that can restrict or expand financial conditions. To combat inflation, the Fed has been aggressively hiking rates to slow demand, which many expected to trigger a recession.[19]

Now a Goldilocks “soft-landing” scenario of falling prices without substantial unemployment has been playing out. The Fed’s preferred measure of inflation, the core personal consumption expenditures index, rose to only 4.1% in June, compared to the estimated 4.2% and marks the lowest annual rate level since September 2021.[20] A resilient job market supported consumer spending, and the US economy grew faster than expected in the second quarter as measured by GDP.[21]

It’s important to note that the Fed would still like inflation to come back down to the 2% target, and timing rate cuts is also critical to a successful soft landing.

Many Fed researchers no longer expect a recession, and Fed chair Jerome Powell expects that the Fed can cool inflation without a large increase in unemployment.[22] Markets are growing increasingly hopeful that the Fed might be able to pull off a soft landing.

Looking Ahead

The Fed still plans to set policy based on incoming data, and Powell noted that “at the margin, stronger growth could lead, over time, to higher inflation, and that would require an appropriate response from monetary policy.”[23]

That opens the door for further interest rate hikes or higher rates for longer, if necessary. The next Fed rate decision will be in September. To complicate matters, measures of financial conditions have actually been easing since last year, coinciding with the equities rally.[24] Recent and upcoming earnings reports may provide more clarity on how companies have been weathering higher rates, though policy effects operate with a lag.

This year’s stock market performance underscores the futility of trying to time the market. Instead, we focus on crafting balanced and diversified portfolios that meet your personal objectives and needs. It’s also worth noting that our portfolios are not likely to match this year’s stock performance exactly — our strategies are typically designed to capture opportunities throughout the market cycle.

Let us know if we can address any questions, discuss recent developments, or talk strategy on a call. We hope you stay hydrated and refreshed for the remaining days of summer!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] July is already the warmest month on record, scientists calculate | AP News

[2] Stock market today: Live updates (cnbc.com)

[3] https://www.bloomberg.com/news/articles/2023-07-29/stocks-crush-year-of-bond-in-biggest-market-sentiment-shift-since-99

[4] Wall St. Pessimists Are Getting Used to Being Wrong – The New York Times (nytimes.com)

[5] Stocks Crush ‘Year of Bond’ in Biggest Market Sentiment Shift Since ‘99 – Bloomberg

[6] Wall St Week Ahead Relentless U.S. stock rally faces Fed test | Reuters

[7] Stocks Crush ‘Year of Bond’ in Biggest Market Sentiment Shift Since ‘99 – Bloomberg

[8] https://www.bloomberg.com/news/articles/2023-07-29/stocks-crush-year-of-bond-in-biggest-market-sentiment-shift-since-99

[9] Economic Data Bolster Soft Landing Hopes – The New York Times (nytimes.com)

[10] S&P 500 Profits Get a Lift From the Crack in King Dollar’s Reign (yahoo.com)

[11] The Benefit of Owning Stocks Over Bonds Keeps Shrinking – WSJ

[12] Putting the income back into fixed income: the return of bonds as an investable asset class – Financial Times – Partner Content by Societe Generale (ft.com)

[13] What the Bank of Japan’s Yield Curve Control Change Means for Global Markets – Bloomberg

[14] What the Bank of Japan’s Yield Curve Control Change Means for Global Markets – Bloomberg

[15] Bank of Japan loosens grip on rates as prices rise, markets bet on bigger pivot | Reuters

[16] Bank of Japan Edges Toward Letting Rates Rise – The New York Times (nytimes.com)

[17] Fed lifts rates, Powell leaves door open to another hike in September | Reuters

[18] Fed lifts rates, Powell leaves door open to another hike in September | Reuters

[19] Wall St Week Ahead Relentless U.S. stock rally faces Fed test | Reuters

[20] PCE inflation June 2023: Yearly rate increase is lowest since March 2021 (cnbc.com)

[21] US economy defies recession fears with strong second-quarter performance | Reuters

[22] https://www.bloomberg.com/news/articles/2023-07-27/us-gdp-growth-accelerates-to-2-4-as-consumers-show-resilience

[23] Economic Data Bolster Soft Landing Hopes – The New York Times (nytimes.com)

[24] Endgame for Fed’s tightening cycle challenged by easing financial conditions | Reuters