The Bumpy Path to Normalization: January 2022 Markets

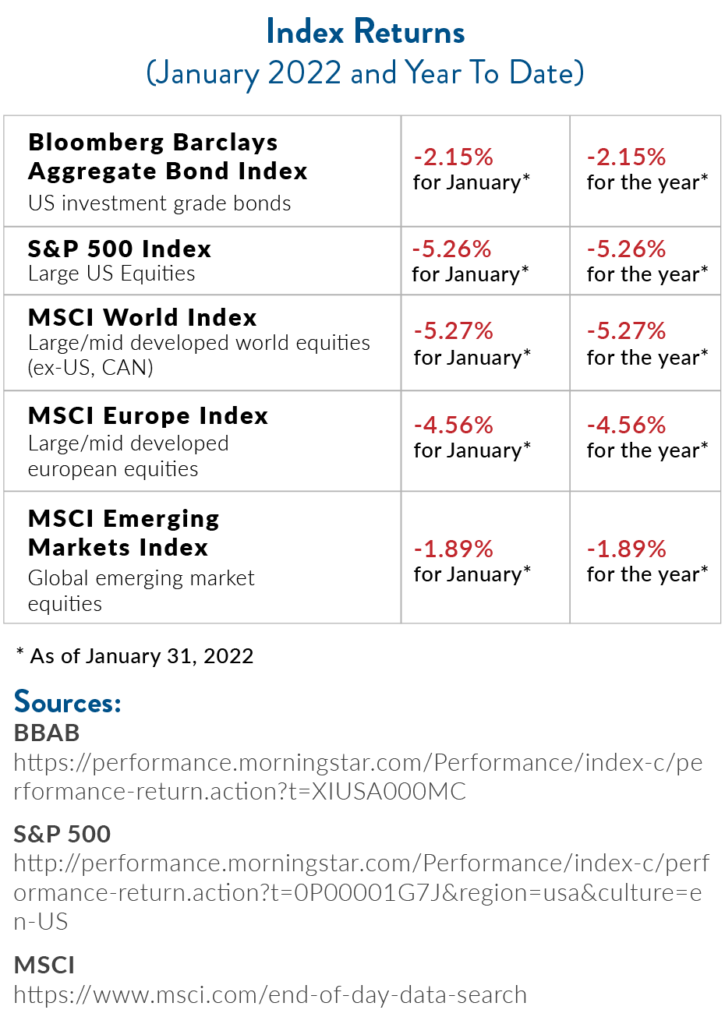

Markets had a rocky January, with the S&P 500 Index posting its biggest January decline since 2009.[2] Bond markets were similarly under pressure, with yields starting the year moving sharply higher, resulting in lower prices.[3] It was a sobering start to the year.

However, the month ended on a positive note. As the broad equity indexes surged to close the month,[4] corporate earnings demonstrated continued strength in the face of higher inflation readings and supply chain issues. Already, 33% of S&P 500 stocks have reported fourth quarter earnings, with growth coming in 24% above expectations year-over-year.[5]

However, the month ended on a positive note. As the broad equity indexes surged to close the month,[4] corporate earnings demonstrated continued strength in the face of higher inflation readings and supply chain issues. Already, 33% of S&P 500 stocks have reported fourth quarter earnings, with growth coming in 24% above expectations year-over-year.[5]

Rate Hikes Are Coming

Rate Hikes Are Coming

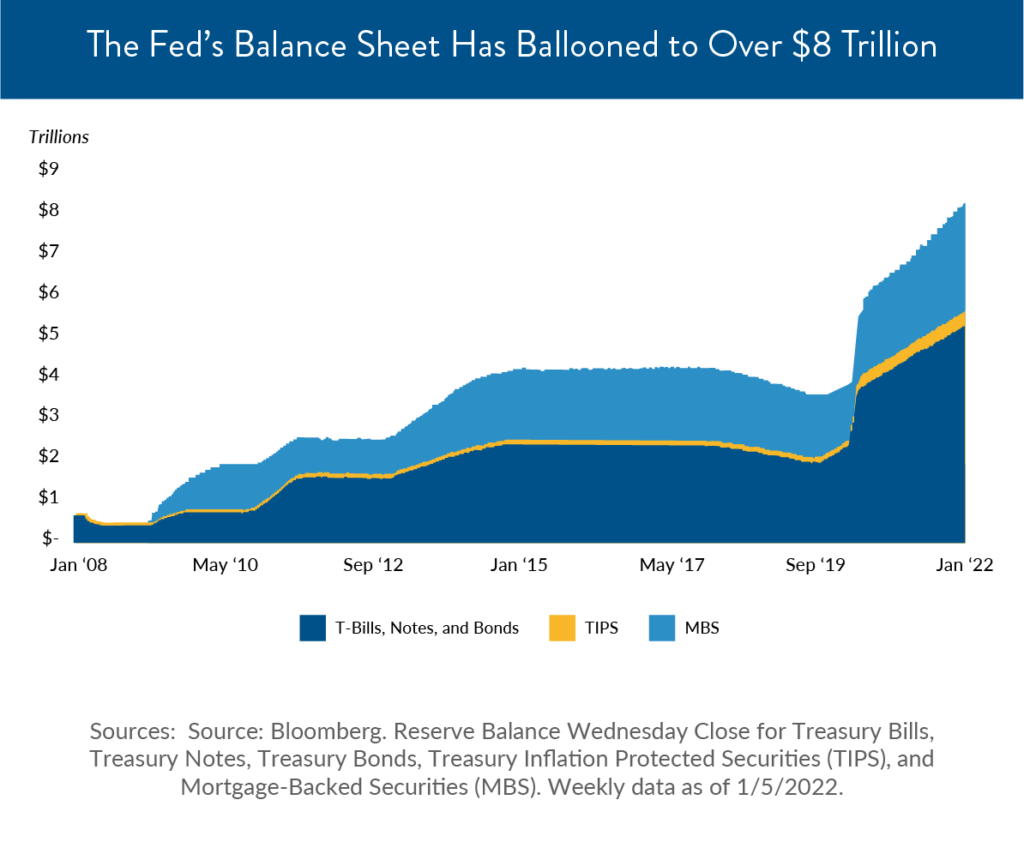

Some of the most significant news of the month came in early January, with the release of the Federal Reserve’s December Federal Open Market Committee (FOMC) meeting minutes. This meeting featured a discussion about shrinking the Fed’s balance sheet in a process known as quantitative tightening (QT).[6] This would follow the end of the Fed’s purchases in the bond markets, removing a layer of liquidity and support for the economy. Some might argue that this move is long overdue: to get a sense of the historical context, the Fed’s balance sheet has ballooned from under $1 trillion in 2008 to over $8 trillion today.[7]

After the meeting in January, U.S. Fed Chair Jerome Powell once again affirmed the Fed’s intention to also begin a series of rate hikes, with the first likely to come in March.[8] He stopped short of indicating whether it would be a 50-basis point rate hike, though he also didn’t rule this out.[9]

Together, these indicators show that the Fed sees very little reason to further delay normalizing policy. Since inflation is running hot at 7% and unemployment is low at 3.9%, this does make sense.[10] However, the idea of combining rate hikes and quantitative tightening roiled bond markets, especially in comparison to how slowly the Fed embarked on quantitative tightening following the 2008 financial crisis.

During the last cycle, the Fed waited a full 2 years after hiking rates to end quantitative easing.[11] Clearly, the economic backdrop has changed significantly, and the economy is in a much stronger place. As such, even though the Fed started discussing an acceleration of rate hikes last year, the markets finally acknowledged and brought forward rate hike expectations, resulting in the repricing of treasury bonds.

As a result, U.S. 10 treasury yields jumped to 1.9%, a new high in the post-Covid world.[12]

Bright Spot Among Bond Markets in Munis

When it comes to bonds, however, a common question we hear from clients is about the stability and safety of municipal bonds—especially in a changing economic environment. Investors might use municipal bonds as a core component of their fixed income portfolio, as they generally offer stable income with tax benefits and typically low default rates.

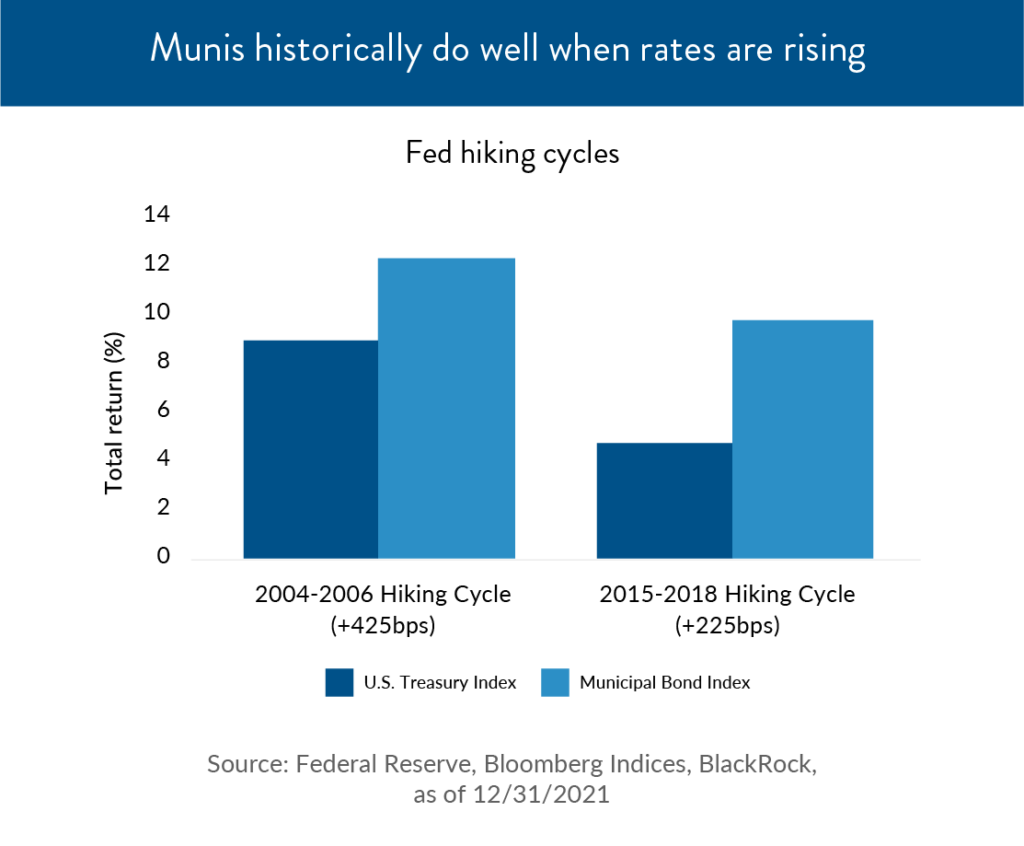

The year 2021 was positive for municipal bonds, as demand continued to be strong, and even in a higher interest rate environment, BlackRock expects low-single-digits returns for investment grade (a low risk of a credit default) municipal bonds.[13]

Overall returns may moderate this year, though municipal bonds tend to do well when interest rates are on an upward swing.[14] We wrote about municipal bonds in more detail in a recent white paper, which we invite you to read on our website.

The Path Forward

So, where do we go from here? There are three main variables that we are watching. The first is inflation, the second is the labor market, and the third is geopolitical tension between Russia and Ukraine.

Inflation will likely settle at levels higher than they were pre-Covid.[15] While supply chains issues could work themselves out pretty soon, it may still take some time to work through these imbalances. However, there are other pressures on inflation, and we believe that we’re likely to see those persist.

The other mandate the Fed has is employment. Even though markets were surprised by the Fed’s recent rate hikes and monetary tightening announcements, there is a silver lining. The Fed feels comfortable moving rate hikes forward because the economy seems close to full employment. That’s good news after the massive pandemic job losses we saw in 2020, even though there are still 3.8 million fewer people working now than before the pandemic.

As far as Russia and Ukraine, we hope that cooler heads will prevail, but the potential conflict is contributing to the rise in oil costs.

In other words, the economic backdrop is strong, and economists generally expect above trend growth in this phase of the recovery, despite perennial geopolitical concerns.[16] Even if market returns are less impressive than they have been in the last couple years, moderation in inflation and growth leaves room for optimism and opportunity.

As always, if there is anything we can do to answer your questions, please don’t hesitate to ask. We are here as your partner to help you navigate through uncertainty and the wobbles and volatility of markets.

Click to view print version of this article.

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Europe Index captures large and mid-cap representation across 15 developed markets countries in Europe and covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 emerging markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

Sources:

[1] https://www.bloomberg.com/graphics/2022-investment-outlooks/

[2] https://www.cnbc.com/2022/01/30/stock-market-futures-open-to-close-news.html

[3] https://www.pimco.com/en-us/insights/blog/rise-in-treasury-yields-may-portend-volatility-in-the-months-ahead

[4] https://www.wsj.com/articles/global-stocks-markets-dow-update-01-31-2022-11643618420

[5] https://www.edwardjones.com/us-en/market-news-insights/stock-market-news/stock-market-weekly-update

[6] https://www.schwab.com/resource-center/insights/content/feds-policy-tightening-plan-one-two-punch

[7] https://www.schwab.com/resource-center/insights/content/feds-policy-tightening-plan-one-two-punch

[8] https://www.cnbc.com/2022/01/26/fed-decision-january-2022-.html

[9] https://www.pimco.com/en-us/insights/blog/the-feds-road-to-full-normalization/

[10] https://www.bloomberg.com/news/articles/2022-01-12/inflation-in-u-s-registers-biggest-annual-gain-since-1982

[11] https://www.schwab.com/resource-center/insights/content/feds-policy-tightening-plan-one-two-punch

[12] https://www.cnbc.com/2022/01/19/us-bonds-treasury-yields-move-higher-as-investors-bet-on-rate-hikes.html

[13] https://www.blackrock.com/us/individual/insights/municipal-monthly

[14] https://www.blackrock.com/us/individual/insights/municipal-monthly

[15] https://www.blackrock.com/us/individual/insights/blackrock-investment-institute/weekly-commentary

[16] https://www.bloomberg.com/graphics/2022-investment-outlooks/

Performance table sources:

BBAB: https://performance.morningstar.com/Performance/index-c/performance-return.action?t=XIUSA000MC