Display results

21 November

Under Pressure

Quick Take: US equities markets corrected as US long-term bond yields rose above 5%.1

Battered US stocks dipped to five-month lows as both the S&P 500 and Nasdaq (down 2.2% and 2.8%, respectively) fell into correction territory after dropping 10% from July highs.2, 3, 4, 5

During the third-quarter earnings season, even though around 75% of companies beat expectations, stocks were disproportionally sensitive to bad news.6 Momentum in tech stocks turned as the Nasdaq 100 erased about a third of its AI-driven advance.7 As we’ve discussed the last few months, stocks have been under pressure because of a sharp rise in bond yields (prices fell).8

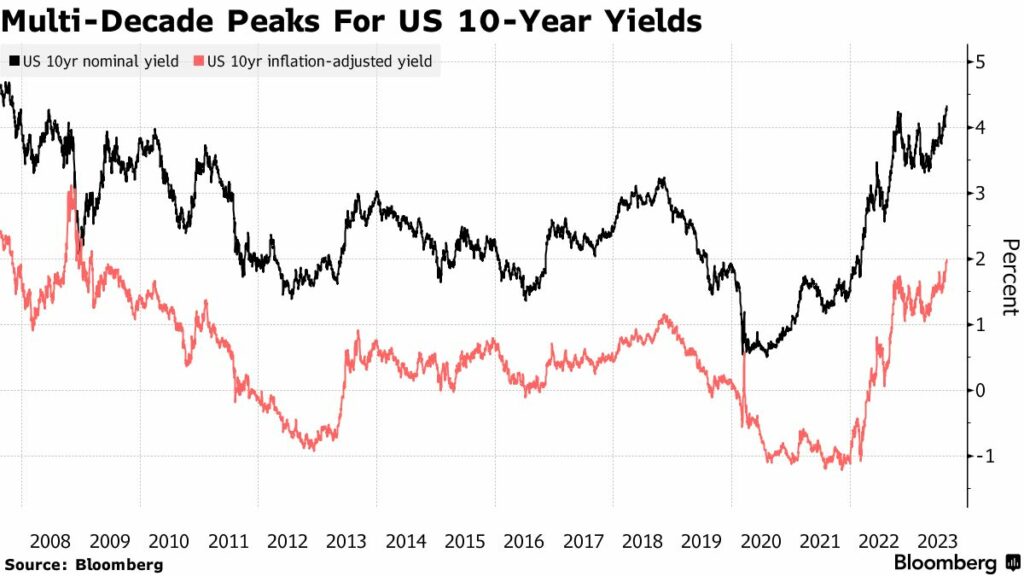

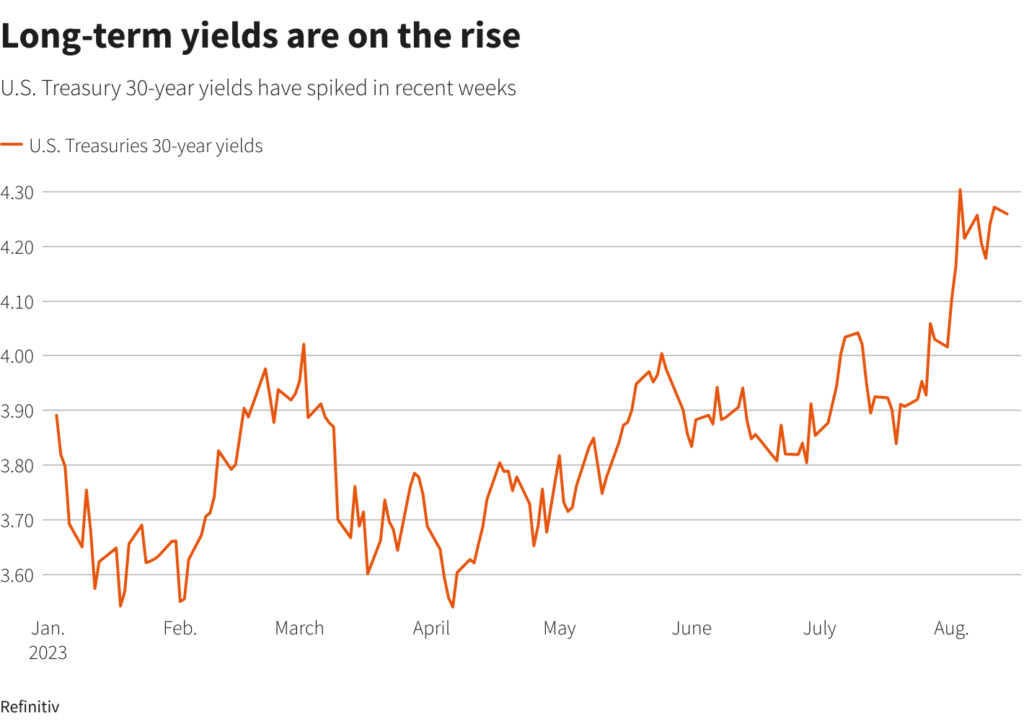

Bond yields softened towards the end of the month (prices rose) after the 30-year bond peaked around 5.18%, and the 10-year surpassed 5% for the first time in 16 years.9 According to Treasury Secretary Janet Yellen, the strength of the economy has driven the rise in bond yields.10

A Strong Economic Pulse

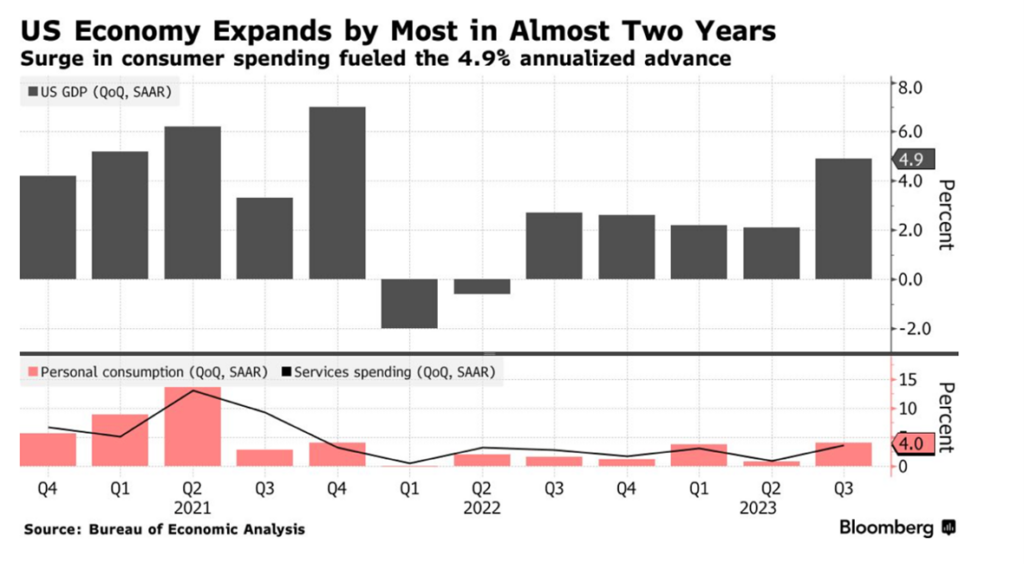

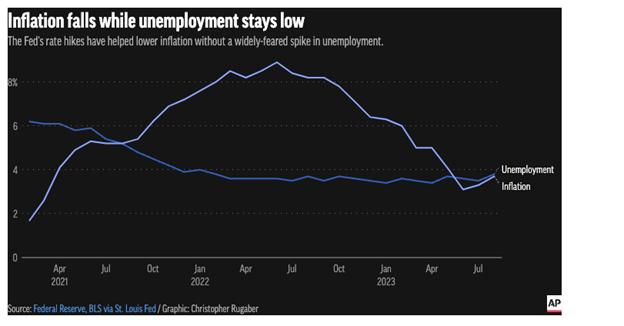

Robust consumer spending drove a stronger-than-expected 4.9% surge in 3rd quarter GDP, the fastest expansion in nearly two years.11 Despite lingering inflation, a tight labor market continues to support household spending, as Americans also borrow and tap into savings.

So why hasn’t the economic strength fueled inflation? US core PCE data, the Fed’s preferred inflation gauge, slowed further in September on falling goods prices.12

Fed Chair Jay Powell noted that despite strong demand, labor supply has also increased, leading to a healthy rebalancing in the employment market.13 In the past year, the labor force grew by about three million people, which is four times the typical long-run rate.14 That’s why wage increases are still coming down.

Geopolitical Tensions

Internationally, tensions have undeniably grown in the global landscape. We are seeing violence from the Israel-Hamas war, a persistent war in Ukraine, and deteriorating U.S.-China relations.15 What has been the impact on markets?

The answer is — outside of local market reactions, not much. The horrors in Ukraine have left the S&P 500 index almost exactly where it was when Putin’s troops invaded.16 Oil and gold have crept higher since the alarming developments in Israel and the Gaza strip, but we haven’t seen a significant “risk-off” move into bonds that might increase prices and depress yields.17 Geopolitical shifts may instead be reinforcing higher interest rates as countries invest in defense spending and reduce trade.18

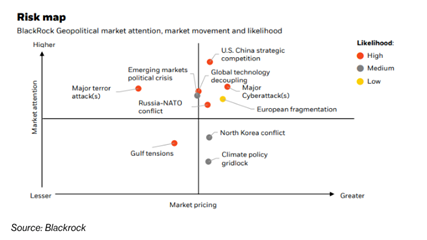

Source: https://www.blackrock.com/corporate/literature/whitepaper/bii-global-outlook-in-charts.pdf

According to BlackRock, strategic competition between the US and China is one of the top geopolitical risks facing markets worldwide.19 Last year, the US began imposing export controls on cutting-edge semiconductors used for AI, and China has retaliated by restricting exports of critical materials for semiconductor manufacturing.20, 21 Nvidia’s Chief Financial Officer noted that long-term export restrictions will result in a permanent loss of opportunities for the US industry and impact future business and financial results.22

This past month, the Biden administration further toughened restrictions on semiconductor exports. However, there are signs that the US and China may try to reboot ties as President Biden and Chinese leader Xi Jinping agreed in principle to meet at a summit in November.23

Historic Deals Tentatively Reached

Talks between the United auto workers and the Big 3 — GM, Ford, and Stellantis — reached a welcome tentative resolution after six weeks of labor strikes. The expected deals secured record concessions for union members with raises, cost-of-living adjustments, and enhanced profit-sharing bonuses.24 The strike has been the longest US auto strike in 25 years, and the deals are waiting for approval by union members.25

Ford noted that the concessions would add $850-$900 in costs per vehicle assembled. However, the finance chief said they would work to “find productivity and cost reductions to deliver on profitability targets.26 Ultimately, their cars must still compete with the rest of the market, including with nonunionized automakers, which means that car prices won’t necessarily see much of an impact.

While putting the final touches on this month’s newsletter, it was announced that SAG-AFTRA’s negotiating committee reached a deal with studios to end an almost four-month-long strike.27 Board members from the actor’s union voted to ratify the agreement, which includes wage increases and controls surrounding the use of artificial intelligence among other items. Union members will now vote on the agreement over the next several weeks.28 The strike caused much pain in the local economy here in Los Angeles as well as beyond, and we hope that the deal leaves both sides satisfied with the result.

Looking Ahead

In the first week of November, the Fed declined to raise interest rates again. Elevated bond yields ease some of the pressure on the Fed to tighten monetary policy, though a final rate hike for 2023 is still possible. Futures markets indicate around a 70% probability that rates will stay the same at the December Federal Open Market Committee (FOMC) meeting.29

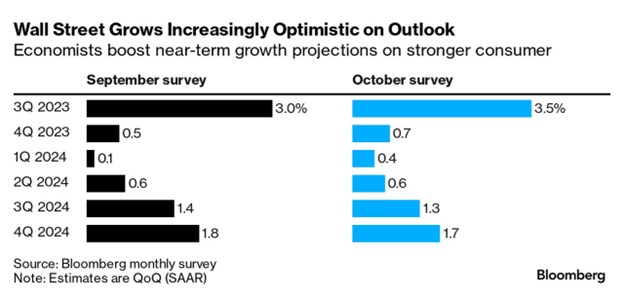

PIMCO believes both growth and inflation have peaked – we may see the economy transition from strength to weakness next year as fiscal support diminishes and the delayed impact of tighter monetary policy materializes.30 Consumer spending also may not be sustainable.

Yet economists have raised US growth projections and lowered odds of a downturn to a one-year low.31

As Schroder’s group chief investment officer Johanna Kyrklund says, valuation matters again – it’s no longer “The fear of missing out (FOMO) but a ‘do your homework’ market.”32

As we navigate the complexities that each new month may bring, we do so with the confidence that comes from a well-thought-out, disciplined investment approach. After all, it’s not about weathering a single storm, but sailing smoothly over decades.

Please reach out if you’ve had any changes in circumstances or goals so that we can make sure your portfolio fits your needs. If you haven’t already, it’s a great time to schedule your year-end review. Wishing you all a Happy Thanksgiving! As we count our blessings, we thank you for trusting us on your financial journey. We are grateful for your continued partnership and confidence through the uncertainty this year has brought us. We hope your day is full of your favorite dishes and memorable time spent with friends and family!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

1 https://finance.yahoo.com/news/ackman-gross-abandon-bearish-bond-191916624.html

3 Nasdaq Correction Could Give Way to Buying Opportunity | Nasdaq

4 Wall St closes higher on eve of Fed decision; investors assess earnings | Reuters

5 Stock market today: Live updates (cnbc.com)

6 US stock market correction: What comes next? | UBS United States of America

7 How Low Can It Go? Getting to the Bottom of the Nasdaq Selloff (yahoo.com)

8US stock market correction: What comes next? | UBS United States of America

9https://finance.yahoo.com/news/ackman-gross-abandon-bearish-bond-191916624.html

10Yellen says US GDP is a ‘good strong number’, may keep bond yields higher (yahoo.com)

11Resilient U.S. economy grew at a ‘stellar’ pace over the summer (msnbc.com)

12Inflation Edges Down in September, in Line With Estimates | Economy | U.S. News (usnews.com)

13Fed Takes Heart in a Supply-Side Boom – WSJ

14 Fed Takes Heart in a Supply-Side Boom – WSJ

15 Markets in an Era of Clashing Superpowers – Bloomberg

16 Markets in an Era of Clashing Superpowers – Bloomberg

17 Markets in an Era of Clashing Superpowers – Bloomberg

18 Markets in an Era of Clashing Superpowers – Bloomberg

19 Geopolitical risk dashboard (blackrock.com)

20 How the U.S. Stumbled Into Using Chips as a Weapon Against China – WSJ

21 U.S. Tightens Curbs on AI Chip Exports to China, Widening Rift With Nvidia and Intel – WSJ

22 U.S. Tightens Curbs on AI Chip Exports to China, Widening Rift With Nvidia and Intel – WSJ

23 U.S., China Agree in Principle to Biden-Xi Summit – WSJ

24 UAW: Winners and losers of 2023 talks with GM, Ford, Stellantis (cnbc.com)

26 UAW: Winners and losers of 2023 talks with GM, Ford, Stellantis (cnbc.com)

28 https://apnews.com/article/actors-strike-deal-d5f9769fd8a263170141a60da64cdc98

29 Live updates: Markets rise after Federal Reserve hits pause again on rate hikes (cnn.com)

30 Cyclical Outlook: Post Peak | PIMCO

31 Bloomberg Evening Briefing: The US Economy Just Had a ‘Stellar Summer’ – Bloomberg

32 Markets in an Era of Clashing Superpowers – Bloomberg

Read more

30 October

A Rocky Month

Quick Take: The Fed signaled continued restrictive monetary policy, prompting bond yields to continue their rise (prices fell). Equities turned in their worst monthly performance for the year, and the US government narrowly averted a shutdown.[1]

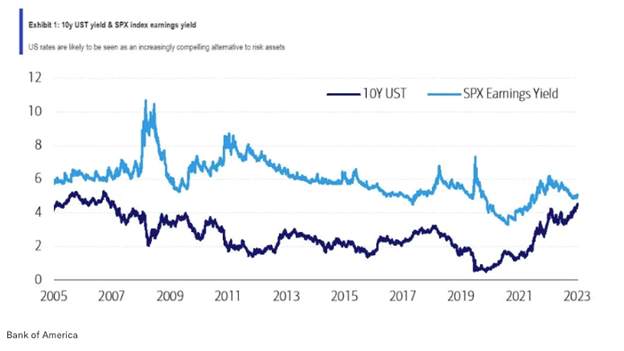

For over a decade since the Great Financial Crisis, an era of near zero-interest rates spawned the mantra TINA “there is no alternative” to stocks. Now, with higher interest rates, the gap between the S&P earnings yield (which shows company earnings received for each dollar invested) and benchmark 10-year Treasury yields is the narrowest it’s been since 2005.[2] That shift is a sign that investors have compelling alternatives to equities.

Source: https://finance.yahoo.com/news/chart-day-forget-tina-hello-020757148.html

One of these alternatives comes from the yield on bonds. Last month, we discussed an increase in longer-term bond yields, a trend that persisted in September. The 10-year Treasury, a key reference rate for loans like mortgages and car loans, experienced its largest monthly jump in a year and hit its highest level since 2007, ending the month at 4.58%, up from 4.09%.[3][4]

The surge in bond yields gives investors an opportunity to earn returns in the bond market with potentially less risk than the stock market, which helped push stocks lower.[5]

Source: https://www.wsj.com/finance/stocks/the-2023-stock-market-rally-sputters-in-new-world-of-yield-63134c7f

What caused the sharp selloff in bonds that spilled over into stocks? The likely culprit was the Fed.

US stocks had been essentially flat heading into the central bank meeting Sep 20-21, but turned lower after officials signaled they might hold rates near current levels through 2024.[6] The S&P and Nasdaq ended September down 4.9% and 5.8% respectively.[7] Heading into the final quarter, the S&P 500 still boasts a 12% performance for the year, while most other market indexes are flat to down year-to-date.[8]

Hawkish Fed

As expected, the Fed didn’t hike interest rates in September but sent a hawkish message with a clear bias toward more restrictive monetary policy.[9]

Along with sharply revising up economic growth expectations for 2023, the Fed released projections that estimate one more rate hike before the end of the year, followed by two rate cuts in 2024, which is two fewer than previously projected in June.[10] [11] That would leave the target fed funds rate around 5.1%.[12]

Fed Chair Jerome Powell noted that the change comes more from optimism about economic growth rather than inflation concerns, though he’d still like to see more progress in the inflation fight.[13]

Inflation progress was validated by the central bank’s preferred inflation measure, the personal consumption expenditures price index, which showed the slowest monthly increase since 2020 in August.[14] The job market is also resilient, with the low 3.8% unemployment rate barely changed since March 2022.[15]

Source: https://apnews.com/article/inflation-jobs-economy-interest-rates-unemployment-recession-7b94da1534f775b08939d184e53ca635

Union Activity

Another sign of job market strength is the increase in major strike activity, helping unions demand better pay and benefits. Strikes with at least 100 or more strikers that have lasted a week or more rose to 56 in the first nine months of the year, up 65% since 2022.[16]

Strikes have occurred across industries. After five months on the picket line, the Writers Guild of America has just reached a deal, winning improved wages and job protections.[17][18] The SAG-AFTRA that represents actors remains on strike but has returned to the bargaining table with Hollywood studios.[19] In healthcare, a coalition of Kaiser Permanente staff are scheduled to go on strike for three days.[20]

Mid-September, the United Auto Workers launched unprecedented, simultaneous strikes at GM, Ford, and Stellantis assembly plants. At the moment, only about 25,000 of the UAW’s 146,000 members are on strike, though the UAW has continued to expand numbers to apply pressure on contract negotiations.[21][22] Lost wages, lower spending, and potentially higher auto costs are potential consequences of the strike, though the severity depends on the length and scale of strikes.

Moody’s Analytics chief economist Mark Zandi estimates that a full-scale UAW strike that lasts six weeks could reduce annualized 4th qtr GDP growth by 0.2%, which is small but meaningful given other potential headwinds from higher rates and gas prices.[23]

The overall impact on the macro economy from strikes may end up being small – just 6% of private sector workers belonged to unions in 2022, which is a record low.[24] Given the substantial rise in inflation that preceded union activity, these strikes probably should not be a massive surprise.

Government Narrowly Avoids Shutdown

Labor strikes weren’t the only source of potential disruption – the government faced a looming shutdown as funding was set to expire at the end of September. Passage of a funding bill was so uncertain that Goldman Sachs put the odds of a government shutdown at 90%.[25]

On the final day Congress had to work out a solution, they passed a bipartisan agreement to keep the government funded until November 17.[26] This makes a near-term government shutdown still possible, and we can probably expect more political wrangling ahead as we have seen discord throughout the political parties.

Looking Ahead

Markets made it out of a historically tough month with a few remaining headwinds. Although the economy has held strong over the summer, monetary policy operates with a lag, and its full impact probably won’t be felt until the end of this year or early 2024.[27] Oil prices hit 10-month highs, and after a three-year pause since the pandemic, millions of student loan borrowers start accruing interest costs again and resume student loan repayments in October.[28][29] The Fed meets again November 1-2 where another rate hike is on the table and bond yields could still go higher.[30]

As we navigate the uncertainty, we have the benefit of perspective gained while managing portfolios through numerous economic cycles. With a disciplined, long-term investment plan, we avoid the pitfalls of reacting to continuous news flow or the urge to time the market (which usually does not end well). As always, we are happy to discuss the markets, our approach, and your portfolio with you – now is a good time to schedule a year-end review. Hope you enjoy a bewitching October with treats (and maybe a few tricks)!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

Sources:

[1] https://www.wsj.com/livecoverage/stock-market-today-dow-jones-09-29-2023

[2] CHART OF THE DAY: Forget TINA, hello TAMA – investors now have plenty of alternatives to the stock market (yahoo.com)

[3] US stocks notch quarterly drop against backdrop of Treasury sell-off | Financial Times

[4] The 10-year Treasury yield: What it is and why it matters (usatoday.com)

[5] Stocks Wrap Up Another Weak September – WSJ

[6] https://www.wsj.com/finance/stocks/the-2023-stock-market-rally-sputters-in-new-world-of-yield-63134c7f

[7] https://www.wsj.com/articles/stocks-have-had-a-great-year-cue-the-september-effect-fa922be9

[8] The 2023 Stock-Market Rally Sputters in New World of Yield – WSJ

[9] Fed rate decision September 2023: Leaves rates unchanged (cnbc.com)

[10] Fed signals it will raise rates one more time this year (cnbc.com)

[11] Fed rate decision September 2023: Leaves rates unchanged (cnbc.com)

[12] Fed rate decision September 2023: Leaves rates unchanged (cnbc.com)

[13] Fed signals it will raise rates one more time this year (cnbc.com)

[14] https://www.wsj.com/finance/stocks/global-stocks-markets-dow-news-09-29-2023-8e039a51

[15] Why the US job market has defied rising interest rates and expectations of high unemployment | AP News

[16] America is on strike. Here’s the progress unions have made | CNN Business

[17] America is on strike. Here’s the progress unions have made | CNN Business

[18] More than 75,000 Kaiser Permanente workers could strike this week – The Washington Post

[19] SAG-AFTRA and studios meet for a second day of bargaining – Los Angeles Times (latimes.com)

[20] America is on strike. Here’s the progress unions have made | CNN Business

[21] UAW strike: Union orders 7,000 more workers to walk off job | AP News

[22] UAW to strike more GM, Stellantis facilities, makes progress with Ford | Reuters

[23] https://www.cnn.com/business/live-news/ford-uaw-strike-stellantis-09-22-23/h_642ecd2f46749a4362d1ff479531f53f

[24] More Labor Strife Is Coming to the US Economy – The Washington Post

[25] https://www.gspublishing.com/content/research/en/reports/2023/09/27/445d5477-1cfc-4015-b441-932e24472720.html

[26] (4) Live updates: House passes bill to avoid a government shutdown, sending it to Senate (nbcnews.com)

[27] Six reasons why a US recession is still likely and coming soon (cnbctv18.com)

[28] Oil prices ease after hitting 10-month highs as investors take profits | Reuters

[29] How resuming of student loan payments will impact the economy | abc10.com

[30] The Fed – Meeting calendars and information (federalreserve.gov)

Read more

14 September

Cooler Days

Quick Take: Bond yields soar (prices fall) as investors predict interest rates will stay higher for longer. Stocks took a breather following months of gains.

Amid a hot year for stocks, markets cooled in August, with major US equity indices closing lower. Following five consecutive months of gains, the S&P 500 and the tech-heavy Nasdaq lost 1.7% and 2.2%, respectively.[1] By the end of August, the S&P 500 was still up 17.4% year to date, with the Nasdaq up a rousing 34.1%.[2]

Source: https://www.wsj.com/finance/investing/the-generational-paradigm-shift-taking-over-markets-e1e7d4e6

Investors continue to spend confidently while believing in the potential for artificial intelligence to boost productivity, but stock markets fell for much of August before turning upward.[3] Treasury bond market gains for the year vanished as longer-term bond prices fell.[4] In this note, we’ll look at a few of the major drivers for last month’s markets.

Fitch Downgrade and Government Funding

August began with an abrupt credit rating downgrade from Fitch Ratings. Weeks after going to the brink of default during debt ceiling negotiations, Fitch Ratings downgraded the US government credit rating from AAA to AA+, citing increasing debt and political dysfunction in Washington.[5] For context, investors typically use credit ratings to evaluate the risk that borrowers such as governments and corporations could default on their debt. US government debt is generally considered the safest, nearly risk-free asset based on the belief in the U.S. government’s ability to pay its bills.

Lower-rated institutions often have to offer higher interest rates to borrow money from investors. However, because investors are unlikely to immediately lose faith in Treasuries as a safe haven, the practical impact of the Fitch downgrade appears minimal. Nonetheless, political stalemates pose ongoing challenges.

The latest political spat looms this fall as a government shutdown could occur as early as October 1 without Congressional approval on spending.[6] A shutdown could affect 4th quarter gross domestic product, which measures economic growth.[7] As with the debt ceiling negotiations, an agreement is still likely, but that doesn’t mean negotiations won’t go down to the wire and heighten market uncertainty.

Jackson Hole

Markets looked to the Jackson Hole Economic Symposium for clarity last month, as central bankers, economists, and financial experts gathered to discuss global economic issues and monetary policy.

The highly anticipated speech by Federal Reserve chair Jerome Powell revealed no major surprises, with Powell holding on to his “higher rates for longer” mantra.[8] Although he acknowledged that inflation has moved down from its peak, he left the door open for future rate hikes, stressing that policy decisions remain data-dependent and promising to “proceed carefully.”[9]

Atlanta Fed President Raphael Bostic says US monetary policy is “already restrictive enough” to reach a 2% inflation target, though that does not spell rate cuts any time soon.[10] Investors are currently betting that the Fed will not make any rate cuts until June 2024.[11]

Bond Yields Surge

Upbeat economic data has already bolstered investor belief that the Fed may sustain higher rates to tame inflation for longer, boosting yields on longer-term government bonds. When yields rise, bond prices fall. Rising rates can also divert demand away from risk assets.

Source: https://www.bloomberg.com/news/articles/2023-08-21/treasury-10-year-real-yield-tops-2-for-first-time-since-2009

Bond yields have been on an upward trajectory in recent months, most recently spurred by higher rates, the increasing size of Treasury bond issuance, and resilient economic data.[12] Investors often demand higher yield compensation as the supply of bonds increases. The surprising strength of the US economy has also played a role.

Despite whispers of an impending recession earlier this year, rising optimism of a soft-landing scenario has instead supported risk assets like equities and high-yield corporate bonds.[13] The latest survey by the National Association of Business Economics shows that almost seven in 10 economists polled are now at least somewhat confident that the Fed will achieve a soft landing.[14]

Source: https://www.reuters.com/markets/us/higher-for-longer-rates-regime-pressures-us-recession-trades-2023-08-16/

In August, benchmark 10-yr Treasury yields rose as high as 4.339%, the highest level since 2007.[15] 30-year Treasury yields similarly spiked on the back of longer-term concerns over US debt sustainability. As yields rose, mortgage rates climbed, topping 7% to levels not seen in 22 years.[16] The ripple effect also extended to increasing rates on auto loans and credit card rates.[17] After years of ultra-low borrowing costs, it may take some time for consumers to adjust to higher rates. Meanwhile, interest rates are finally rewarding savers with increased income.

Higher rates that slow growth and inflation may also lower the need for additional rate hikes, prompting many to believe that the Fed is done with rate hikes.[18]

What’s Next?

The next Fed meeting occurs in September, which is a month without corporate earnings to push stocks higher.[19] We also wouldn’t be surprised to see headlines saturated with political drama from ongoing budget talks.

A potential source of volatility comes from the Sept. 14 expiration of the United Auto Workers contract with the big 3 Detroit automakers. The U.A.W. president was elected last year on a platform to take a more combative and confrontational approach to talks than his predecessors. Labor unions across industries have been pushing for better working conditions and salary raises while displaying a willingness to walk out on the job. An auto strike could cost billions, and companies argue that concessions reduce corporate profitability and competitiveness.[20] However, organized labor, from port workers to UPS employees, have found success this year in renegotiating contracts with better benefits.[21] [22]

On the home front here in Los Angeles, we would be remiss to not mention the ongoing Hollywood writers’ strike – which officially began on May 2, 2023 and hit it’s 100-day mark back in August.[23] Despite SAG-AFTRA joining the WGA with a strike of its own on July 13, there has been seemingly little movement on either side of the picket line toward a resolution. [24] According to recent data from the U.S. Bureau of Labor Statistics, the entertainment industry alone has seen approximately 17,000 jobs lost due to the strike so far, combined with the ongoing SAG-AFTRA strike.[25] This strike has a ripple effect that spans far outside the entertainment community and touches a variety of industries in the local and state economy like dry cleaners, restaurants/food service, real estate and many more.[26] It is impossible to know the true economic impact of the strike as it is still unfolding, but we will continue keep a close eye on progress and hope a resolution will be reached soon.

Looming uncertainty may be unsettling, but as we highlight the unknown, the goal is not to raise concerns or trigger rash decisions. Basing investment decisions on daily or monthly news headlines is more likely than not to land you in hot water. As Vanguard founder John Bogle has said: “Time is your friend, impulse is your enemy.” [27]

We pride ourselves on a durable, strategic focus on wealth management that offers long-term predictability through inevitable ups and downs. Please feel free to reach out if you’d like to discuss the markets, your investment priorities, tax payments and financial needs. We are committed to supporting you and your personal objectives.

We hope everyone enjoyed the unofficial end of summer – and for those who embarked on 1st days of school recently, we wish you a great academic year ahead!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] https://www.investopedia.com/dow-jones-today-08312023-7964094

[2] How major US stock indexes fared Thursday, 8/31/2023 | AP News

[3] Stock Market’s August Losses Snap Monthslong Winning Streak – WSJ

[4] Treasury Market 2023 Gains Vanish as Long-Dated Yields Rise (yahoo.com)

[5] https://www.wsj.com/articles/fitch-downgrades-u-s-credit-rating-56c73b89

[6] White House asks Congress for short-term funding to avoid shutdown (cnbc.com)

[7] A Government Shutdown Could Be Months Away—Here’s How It Would Further Roil Markets After Fitch Downgrade (forbes.com)

[8] Analysis: Powell’s ‘higher for longer’ mantra fans investor caution over economy | Reuters

[9] Fed Chair Powell calls inflation ‘too high’ and warns that ‘we are prepared to raise rates further’ (nbcnews.com)

[10] Atlanta Fed’s Bostic Sees U.S. Policy as ‘Restrictive Enough’ (wsj.com)

[11] Treasury yields and dollar rise after Jay Powell warns on inflation | Financial Times

[12] US Ramps Up Debt Issuance, Adding Fuel to Selloff in Treasuries – Bloomberg (US Treasury ramps up debt issuance, announces it will sell $US103b of longer-term securities (afr.com))

[13] Higher-for-longer rates regime pressures US recession trades | Reuters

[14] US economy poses key question: Are we facing higher-for-longer interest rates? | AP News

[15] https://www.wsj.com/finance/stocks/rising-long-term-rates-loom-over-autumn-on-wall-street-3ee03b95

[16] https://www.wsj.com/economy/housing/mortgage-rates-hit-7-23-percent-72688ccd

[17] US economy poses key question: Are we facing higher-for-longer interest rates? | AP News

[18] US economy poses key question: Are we facing higher-for-longer interest rates? | AP News

[19] Stocks Have Had a Great Year. Cue the September Effect. – WSJ

[20] AEG analysis: UAW strike cost estimated at $5 billion in 10 days (cnbc.com)

[21] US West Coast port workers ratify contract agreement | Reuters

[22] UPS workers approve new contract with hard-fought gains, ending strike threat (nbcnews.com)

[23] https://www.forbes.com/sites/antoniopequenoiv/2023/08/09/hollywood-writers-strike-heres-a-timeline-of-what-led-to-the-100-day-mark/?sh=5524d47c7ad3

[24] https://www.forbes.com/sites/antoniopequenoiv/2023/08/09/hollywood-writers-strike-heres-a-timeline-of-what-led-to-the-100-day-mark/?sh=5524d47c7ad3

[25] https://www.hollywoodreporter.com/business/business-news/writers-strike-update-union-studios-break-off-amptp-1235585993/

[26] https://finance.yahoo.com/news/hollywood-writers-strike-creates-ripple-effects-across-californias-economy-other-states-204742894.html?guccounter=1&guce_referrer=aHR0cHM6Ly93d3cuZ29vZ2xlLmNvbS8&guce_referrer_sig=AQAAANxnOTMpucgupEN6rwCUPHOtp1Umk-1BzDm5ZGPK7U08Cvlv-pFqCluYvvPN7ErSv6R1eyaRBIdF-Qas-Llb08WM9l-ovZ64teql3QqZpQmyZozUaFjUq-2GtL-cXvbDeYSezZIp-cuNf26G1pmuC6Xn-akkgc4QajZ2EdRZLV4U

[27] https://www.cbsnews.com/news/john-bogles-10-rules-of-investing/

Read more