Defying Expectations

Quick Take: Stocks and bonds defied expectations in 2023 as stocks soared and volatile bonds ended up nearly where they started the year.[1]

Flash back to the start of 2023, and the mood across markets was glum. Analysts, expecting a looming recession, advised a shift away from stocks towards the relative safety of bonds.[2] To the surprise of many, expert consensus predictions ended up being dead wrong.

Source: https://www.bloomberg.com/news/articles/2023-12-28/stock-market-today-dow-s-p-live-updates

As a reminder, we were right on the heels of 2022 – a far more challenging year, which had just ended with a dismal record – the worst year in more than a decade for global equities and bonds.[3] The benchmark S&P 500 equity index shed 19.4% for the year, losing roughly $8 trillion in market cap.[4] Tech-heavy Nasdaq saw heavy losses, losing a third of its value. Bonds were also not spared, with Treasuries and corporate bonds logging miserable returns as the Bloomberg Aggregate US Bond Index had its worst year since its inception in 1977.[5] Treasury yields rose (prices lower) on the final trading day, with the 10-year US Government Bond rate touching a seven-week high.[6]

Despite Wall Street’s understandably cautious outlook heading into 2023, the S&P 500 equity index gained 24% in 2023, while the tech-heavy Nasdaq soared 43%, its biggest surge since the dot-com boom in 1999.[7],[8] By the end of December, the S&P 500 had traded close to its all-time high.[9]

In 2023, stocks were fueled largely by excitement over the potential growth in artificial intelligence and growing bets that the Federal Reserve would start cutting rates.[10] Declining interest rates and lower bond yields typically lead to higher bond prices. A drop in yields also takes some pressure off steep borrowing costs.

Source: https://www.reuters.com/markets/rates-bonds/biggest-two-month-rally-decades-rescues-beaten-up-bond-markets-2023-12-28/

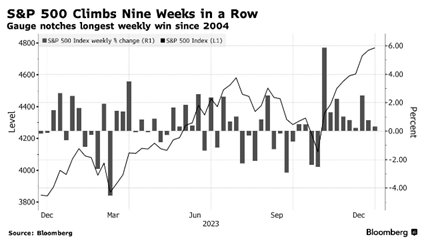

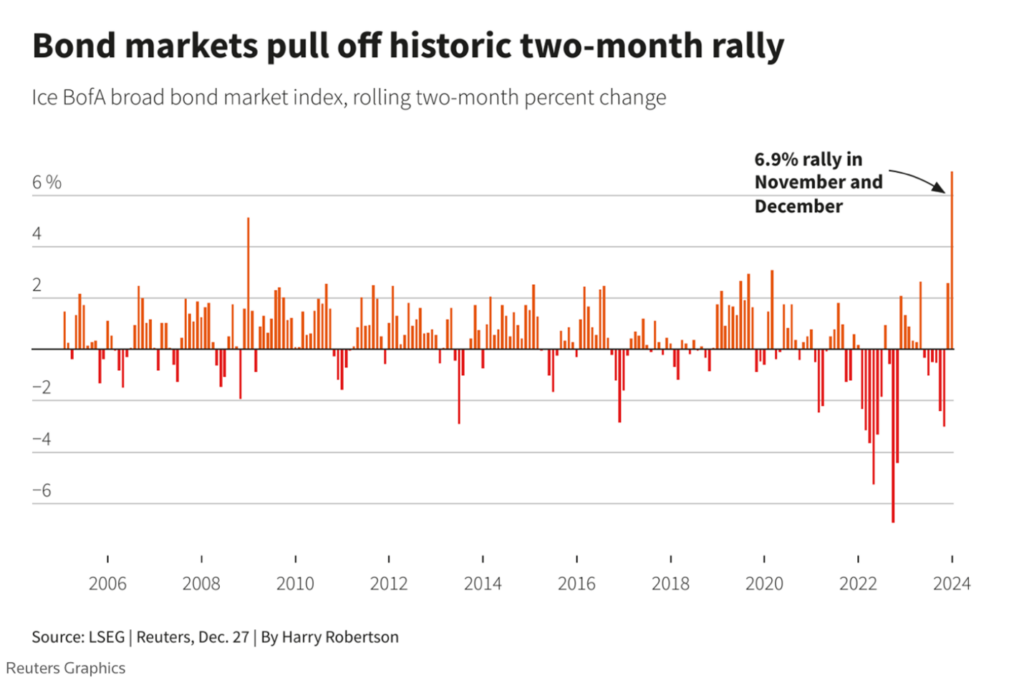

As the year drew to a close, markets enjoyed a spirited Santa rally. To cap off a stellar year, stocks climbed nine weeks in a row while bond markets pulled off its biggest two-month rally in decades.[11]

Holiday Sales: Consumers Shine

In a year of upside surprises for stocks and the economy, the strength of the consumer was noteworthy.

Stronger household finances since the pandemic’s onset have so far provided a buffer against higher borrowing costs. Between 2019 and 2022, median inflation-adjusted family wealth across all demographics and income groups soared 37% – a historic leap.[12] Thanks in part to Congressional relief programs, many families saved and reduced debt. Debt burdens, as a percentage of income or wealth, are near historic lows.[13]

Consumers have kept spending. U.S. retail sales rose more than expected in November, signaling a healthy start to the holiday shopping season.

According to data from Mastercard SpendingPulse, online and in-store retail sales from Nov.1 to Dec 24 grew 3.1% from the previous year.[14] Sales were strong amid deep discounting, and spending at restaurants also rose 7.8% over the same period.[15],[16] The numbers are not adjusted for inflation. A robust consumer is likely to keep the economy on track for moderate growth to end the year.

Peak Rates and a Pivot

Amidst this backdrop of consumer strength, confidence has been growing that the U.S. economy is headed towards a relatively stable and gradual slowdown – in other words, the elusive “soft landing.”

In response to declining inflation, the Federal Reserve (‘Fed”) kept its policy rate steady at 5.25% – 5.5% in its December meeting.[17] At the same time, Fed officials released increasingly optimistic economic projections that inflation would moderate faster with only a modest increase in the unemployment rate.[18] After all, the data is headed in the right direction — consumer prices actually fell in November on a monthly basis for the first time in over three years, according to the Fed’s preferred inflation gauge.[19]

The Fed meeting marked a clear shift. Officials now appear more optimistic about achieving sustainably lower inflation, which has led them to discuss the conditions that would trigger rate cuts. Rate cuts would bring relief from borrowing costs that climbed to its highest levels in a decade in October.[20] While reducing inflation back down to 2% is the goal, the Fed currently doesn’t expect this to happen until 2026.[21]

The equities rally has drawn strength recently from speculation that rate cuts would begin by mid-2024.[22] Fed estimates indicate 75 bps of rate cuts for 2024, up from the previously anticipated 50 bps.[23] In fact, markets have been pricing in earlier and deeper rate cuts of up to 150 bps for the year.[24]

Labor Market: The Backbone of Economic Resilience

As talks of rate cuts swirl, the spotlight remains on the resilient workforce. A firm labor market could keep services inflation afloat. But a robust jobs market also offers crucial support for the Fed’s tightrope walk towards a soft landing.

Economists expect the US Labor Department to report that the unemployment rate held below 4% in December for the 23rd consecutive month – a feat not seen since the 1960s.[25] This rock-solid employment picture comes hand-in-hand with wage growth outpacing inflation, especially for lower-income earners. Rising productivity could also sustain wage gains above pre-pandemic levels.

What’s Next

Going into 2024, the mood may be rosier, but growth will likely slow. Bloomberg Economics forecasts 2024 could be the weakest non-crisis year since the early part of the century.[26] Monetary policy tends to operate with a lagged effect, and it’s difficult to assess when the full weight of higher borrowing costs will be felt. Higher debt costs and lower credit availability could put a dent in future spending.

Source: https://www.bloomberg.com/news/articles/2023-12-22/euphoria-on-pivot-prospects-ignores-the-lagging-hangover-that-will-hurt-economy

Looking back on the past year with the benefit of 20/20 hindsight, we’re reminded that markets are as variable as they are fascinating. That’s why our approach prioritizes a disciplined, long-term approach over crystal ball gazing. We believe in building resilient portfolios to withstand turbulence, so you can embrace the ride without fearing the next turn.

The new year is often a good time for reflection, revisiting and modifying goals, planning for the known, and preparing for the unknown. As always, please reach out if you have had a change in your financial objectives or circumstances. We are always here to support you and are excited to see what lies ahead. Wishing you a new year filled with good health and happiness!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] Shares dip to cap stellar year; Treasuries end volatile 2023 flat | Reuters

[2] ‘Everyone Got Burned’: Wall Street Missed the Great Stock Rally of 2023 (yahoo.com)

[3] https://www.jsffinancial.com/december_2022_markets/

[4] https://www.jsffinancial.com/december_2022_markets/

[5] https://www.jsffinancial.com/december_2022_markets/

[6] https://www.jsffinancial.com/december_2022_markets/

[7] Global markets kick off the new year on lackluster note (yahoo.com)

[8] ‘Everyone Got Burned’: Wall Street Missed the Great Stock Rally of 2023 (yahoo.com)

[9] https://finance.yahoo.com/news/asia-stocks-tread-water-p-224046345.html

[10] AI Mania Driving Nasdaq 100’s Best Run Since 1999: Markets Wrap (yahoo.com)

[11] Biggest two-month rally in decades rescues beaten-up bond markets | Reuters

[12] Labor Will Keep the US Economy Out of a Recession in 2024 – Bloomberg

[13] Labor Will Keep the US Economy Out of a Recession in 2024 – Bloomberg

[14] Holiday Spending Increased, Defying Fears of a Decline – The New York Times (nytimes.com)

[15] Holiday Spending Increased, Defying Fears of a Decline – The New York Times (nytimes.com)

[16] US economic data points to ‘real momentum’ for 2024, White House says | Reuters

[17] Fed’s Dovish Pivot Reflects Lessons From History | PIMCO

[18] Fed’s Dovish Pivot Reflects Lessons From History | PIMCO

19] Interest rate cuts and a soft landing: This will be a critical year for the Fed | CNN Business

[20] Biggest two-month rally in decades rescues beaten-up bond markets | Reuters

[21] Interest rate cuts and a soft landing: This will be a critical year for the Fed | CNN Business

[22] Five Things to Look For in US Stocks in 2024 as S&P Nears Record – Bloomberg (Five things to look for in U.S. stocks in 2024 as S&P nears record | Economy | unionleader.com)

[23] Fed’s Dovish Pivot Reflects Lessons From History | PIMCO

[24] Five Things to Look For in US Stocks in 2024 as S&P Nears Record – Bloomberg

[25] Labor Will Keep the US Economy Out of a Recession in 2024 – Bloomberg

[26] https://www.bloomberg.com/news/articles/2023-12-22/euphoria-on-pivot-prospects-ignores-the-lagging-hangover-that-will-hurt-economy