What Can We Expect in 2021?

A Look at Economic Stimulus & Beyond

Introduction

The world changed in 2020, and there are a number of potential policy measures coming in 2021. In this paper, we’ll take a quick look at economic stimulus and address some questions around what this could mean moving forward.

As always, we are available to you for personal discussions on these issues. While new policies can have broad effects on all of us in some ways, the specific implications for you and your family might be unique. That’s why it is such a high priority for us to plan ahead with you individually, especially at the beginning of the calendar year and a new administration.

As it’s impossible to gauge what will happen, this paper instead outlines some of what might happen. It’s by having a sense of the possibilities that we’re able to draw up contingency plans and risk management frameworks for your wealth and future goals.

Thank you, as always, for your support and trust in our firm.

Jeff Fishman

Stimulus & The Economy

With our focus on policy in this short paper, we won’t go into an extensive review of economic projections but rather some of the key issues facing policymakers in 2021—and the impact that key policy proposals might have moving forward. Chief among those are the Biden stimulus plan and the state of American consumers, who are a critical contributor to economic growth.

Employment & Consumer Health

The American economy lost 140,000 jobs in December, with the unemployment rate holding at 6.7%.[1] Job losses were concentrated in areas most impacted by business closures, namely restaurants, bars, and related sectors. The American economy has over 9 million fewer jobs than it did before the pandemic took hold in March 2020.

A broader way of looking at the unemployment rate includes workers who are underemployed or have grown discouraged in their job search. By including these workers, the unemployment rate rises to 11.7%, which gives you an idea about the broader impact of the pandemic on the availability of jobs.[2]

That said, you have probably heard about the divergence between higher-income earners and lower-income earners with respect to job growth and employment.[3] The leisure and hospitality sectors, which employed 11% of workers in the U.S. as of February 2020,[4] had recovered only about 50% of lost jobs in November (before new winter closures).3 The sector also pays some of the lowest employee wages, potentially magnifying the impact of those losses.

On the other hand, employees in sectors like information services, who make an average of 50% more than other private sector employees, experienced far fewer job losses and recovered them faster. 3

Consumers are also saving more money. The personal savings rate (across all consumers) was 12.9% in November, well above the 7.7% from the fourth quarter of 2019.[5] In other words, people are hanging onto more of their income—whether through need, fear, or simply a lack of things to do and places to spend it.

Put together, it’s clear to us that broad distribution of COVID-19 vaccines will be critical for providing access to jobs and stimulating consumer spending. Another key part of this equation is teachers and the broader ability for schools to reopen.

As of January 12, a Johns Hopkins survey found that 37 out of 51 jurisdictions (the 50 states plus Washington, D.C.) included teachers and/or school staff in Phase 1 vaccination prioritization. Most often, teachers are part of Phase 1b, after high-risk and essential workers. In December, only 23 jurisdictions prioritized teachers in Phase 1. [6]

Of course, vaccination plans are subject to change—and the availability of vaccine supply and the logistical support to administer injections are also critical factors. That said, it does make sense that teachers come earlier in vaccination schedules, not only for educational reasons, but to make it easier for parents to return fully to work (remotely or out of the house.)

To date, the majority of vaccines have gone to essential healthcare workers and the elderly, meaning that it could be some time before enough “non-essential” working-age people are vaccinated to make full reopening a reality. What happens to incomes and savings rates once reopenings begin again will be a major clue in helping us understand how quickly the economy can recover from the pandemic.

The American Rescue Plan

The Biden administration has expressed interest in reviewing, changing, or implementing a number of key economic and tax policies. However, most prominent in the immediate term is the American Rescue Plan, a legislative proposal that seeks to provide additional support for the U.S. economy in the wake of the pandemic.

The $1.9 trillion package follows the $900 billion support bill passed in December. Key target areas of the proposed plan include the following:[7]

● A national vaccination program that establishes vaccination sites, contact tracing, and supply management

● Direct and logistical support for state and local governments

● School investments with the intention of “safely reopening” K-8 schools within 100 days

● Support to Americans via $1,400 checks to individuals and the expansion of direct nutrition/housing assistance, childcare support, minimum wage increase, and expanded unemployment benefits

● Financial support for small businesses and essential workers

Of course, it’s important to remember that this plan is an opening salvo in a longer negotiation within Congress. Realistically, it’s probable that the eventual stimulus will be more generous than it might have been with a Republican-controlled senate, but more modest than what Biden has proposed.

This policy proposal is essentially phase one of two; the Biden administration has indicated that it plans to propose follow-up legislation that focuses on infrastructure investment, including sustainable energy investment and support for U.S. manufacturing capabilities.

Implications of Stimulus

Two key questions our clients have asked: first, what is the impact of higher national debt on the future of our economy? Second, what should we expect around inflation?

The Question of Debt

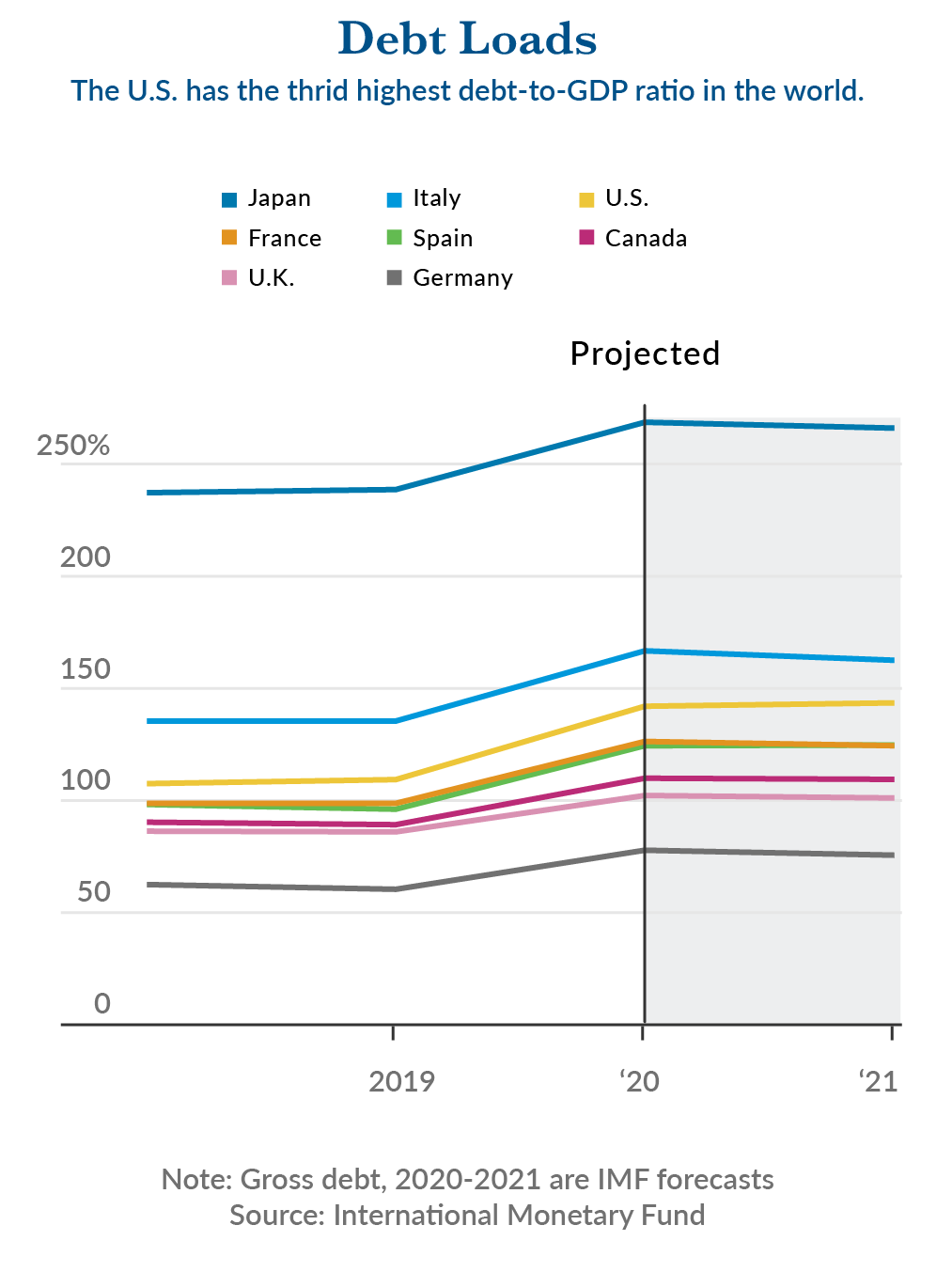

The U.S. entered its 2021 fiscal year in October with the third highest debt-to-GDP ratio in the world, exceeding 100% of GDP for the first time since World War II.[8] GDP, or Gross Domestic Product, is a measure of a nation’s economic output.

The borrowing spree is, yes, comparable to a war effort. Similar to the financial crisis, an approach of strong, emphatic support was put to use already in March 2020, with the CARES Act.

Does this put our country on weaker footing? Right now, debt is incredibly cheap, and demand for American debt has remained strong, so we do not think that there is an imminent problem. That said, debt has to be paid for somehow: either with growth or through fiscal policy (meaning higher taxes or lower spending). The U.S. still occupies rarefied territory on this front, in the sense that the arithmetic is a little different due to the size and influence of the economy and the position of the U.S. dollar as the world’s reserve currency and safe haven.

It could be argued that the trajectory of American deficits is critical: at some point, the debt burden may get too high. We’ll have to see how the American Rescue Plan evolves in Congress and what, if any, follow-on support measures are considered and passed.

Inflation Concerns

One of the reasons for our more detailed discussion of employment above is that jobs and inflation are often tied. Generally speaking, a “tight” labor market, where there is a scarcity of workers, is an important ingredient in inflation. When businesses compete for employees, wages go up, and so goes inflation.

However, right now, we have a large amount of “slack” in the labor market, meaning a lot of potential for jobs growth and a lot of people out of work.

That said, we could see prices in certain areas jump as pent-up demand is unleashed—we can probably all relate to the desire to take a vacation, go to our favorite restaurants, or see a sporting event. A Bloomberg survey of economists found that there is a general expectation we could see a temporary rise of inflation above 2% later in 2021, before the numbers settle right around that area.[9]

This is especially the case because the “base rate” numbers, or the comparison points for 2021 inflation, will include some of the rock-bottom numbers we saw in the spring of 2020, when business closures pushed price levels down.

This is especially the case because the “base rate” numbers, or the comparison points for 2021 inflation, will include some of the rock-bottom numbers we saw in the spring of 2020, when business closures pushed price levels down.

Should we be worried about “stagflation,” or high inflation combined with high unemployment? From our point of view, no, not yet. While, for example, housing prices are up—in some cases quite significantly—so too is the ability for a large number of workers to work from home. Some businesses are making these changes permanent, and even offering workers reduced wages to live in cheaper cities.[10]

While it’s certainly a possibility that the overall trend will surprise us, we think it’s far more prudent to monitor the data rather than relying on speculation or trying to take lessons from other historical situations.

Conclusions

There is clearly stimulus on the horizon, as well as a broader focus on equity in economic policy. We do anticipate some form of economic stimulus, and as we’ve said before, we expect this to be closer to Biden’s vision than what might have been passed under a Republican Senate. However, the breadth and speed of that stimulus remains to be seen.

In terms of the economy, it would not surprise us to see some bumps and wobbles throughout 2021. The reality is that this is an extreme situation, and with the data from 2020 being as grim as they were, we might get the occasional shock in the numbers. Over the longer term, there are a number of policy measures and trends that could temper concerns around debt and inflation.

All in all, our position of prudence, patience, and a longer-term strategic outlook remain. And as always, we encourage you to reach out with questions, comments, and concerns so that we can help you build not only a strategic plan for your wealth, but one which is sustainable and comfortable for you.

Securities are offered through Mid Atlantic Capital Corporation (“MACC”), a registered broker dealer, Member FINRA/SIPC.

Investment advice is offered through JSF Financial, LLC, which is not a subsidiary or control affiliate of MACC.

Confidentiality Note: This email communication, including all attachments transmitted with it, may contain confidential information intended solely for the use of the addressee. If the reader or recipient of this communication is not the intended recipient, or you believe that you have received this communication in error, please notify the sender immediately by return email or by telephone at (323) 866-0833 and PROMPTLY delete this email including all attachments without reading them or saving them in any manner. The unauthorized use, dissemination, distribution, or reproduction of this email, including attachments, is strictly prohibited and may be unlawful.

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of Mid Atlantic Capital Corporation (MACC). Neither JSF Financial LLC nor MACC gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed, constitutes a solicitation or recommendation for the purchase or sale of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC, or MACC as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges, and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

Sources:

[1] This section: https://www.bloomberg.com/news/articles/2021-01-08/u-s-jobs-recovery-faltered-in-december-amid-virus-surge?sref=c4RUGNV1

[2] Source: https://fred.stlouisfed.org/release/tables?eid=4773&rid=50

[3] A summary of data on this issue: https://www.bloomberg.com/news/articles/2020-12-10/how-a-k-shaped-recovery-is-widening-u-s-inequality-quicktake?sref=c4RUGNV1

[4] Source: https://www.fb.org/market-intel/leisure-and-hospitality-woes-a-harbinger-of-employment-trouble-to-come#:~:text=With%20nearly%2017%20million%20jobs,representing%2011%25%20of%20U.S.%20employment.

[5] Source: https://www.bea.gov/news/2020/personal-income-and-outlays-november-2020 and a review of pre-pandemic savings behavior here: https://www.marketwatch.com/story/heres-the-reason-americans-are-saving-so-much-of-their-income-2020-02-18

[6] Source: https://bioethics.jhu.edu/news-events/news/how-are-teachers-prioritized-for-covid-19-vaccination-by-the-us-states/

[7] Source: https://buildbackbetter.gov/wp-content/uploads/2021/01/COVID_Relief-Package-Fact-Sheet.pdf

[8] Source: https://www.wsj.com/articles/u-s-debt-is-set-to-exceed-size-of-the-economy-for-year-a-first-since-world-war-ii-11599051137

[9] Source: https://www.bloomberg.com/news/articles/2020-12-07/get-ready-for-the-great-u-s-inflation-mirage-of-2021?sref=c4RUGNV1

[10] A couple of news pieces on this possibility: https://www.bloomberg.com/news/features/2020-12-17/work-from-home-tech-companies-cut-pay-of-workers-moving-out-of-big-cities?sref=c4RUGNV1 and https://www.bloomberg.com/news/articles/2020-07-23/remote-work-means-pay-cuts-for-white-collar-workers-in-nyc?sref=c4RUGNV1