January 11 2021 Market Update

Snapshot of the Economy

While December brought an immense amount of news to markets and market-watchers, the end of 2020 has easily been overshadowed by political events in the first week of January. Like you, we are watching this historic period unfold in real-time.

That said, there is one issue which we feel able to reasonably assess, and that is the result of the Georgia Senate runoff elections.

With Democratic victories for both Senate seats, the Democratic party now has a majority in Congress, which could have a significant impact on fiscal policy in the coming year.

Please keep an eye out: we’ll assess this issue in more detail in an upcoming coming white paper.

In the meantime, this newsletter will provide you with some context for markets and the economy as we open this New Year.

Year-end snapshot

Overall, economists expect weak growth in the first quarter of 2021, followed by a more rapid return to growth throughout the rest of the year.[1] This, of course, could be highly influenced by the amount of economic stimulus that comes out of Washington, D.C. in the coming months.

Overall, economists expect weak growth in the first quarter of 2021, followed by a more rapid return to growth throughout the rest of the year.[1] This, of course, could be highly influenced by the amount of economic stimulus that comes out of Washington, D.C. in the coming months.

Policy measures notwithstanding, these projections also depend in part on the implementation of COVID-19 vaccinations both here and abroad. As of December 31, 2020, a little over 3 million doses had been given to Americans and 10 million worldwide.[2]

This is one variable in the economic outlook that will simply have to be monitored: not only due to the potential business closures that could result but with respect to the perceptions that consumers have about their ability to return to (both health-wise and economically) their pre-pandemic lifestyles.

Unemployment and the labor market

The unemployment situation steadily improved throughout 2020 but stalled again in December.[3] Employers cut 140,000 jobs in December, the first such decline since the spring. The unemployment rate remained at 6.7 percent. All that in mind, the year closed with employment down by 10 million jobs since February; at the peak, 22 million jobs were lost due to the pandemic.

A major driver of job losses were business closures in the restaurant, hospitality, and leisure sectors. Other sectors added jobs, namely retailers, factories, and construction firms. Government aid for businesses was also temporarily phased out before the December 28, 2020 stimulus was passed into law.

What can we expect going forward?

While much remains to be seen with respect to vaccinations and federal legislation, we think it’s possible that we’ll see additional job losses in the first quarter before things turn around. Again, it’s an important variable to keep an eye on as we work through the coming months.

Markets

It wasn’t just the pandemic and the economy that were unique to 2020: the markets surprised more than a few people as well.

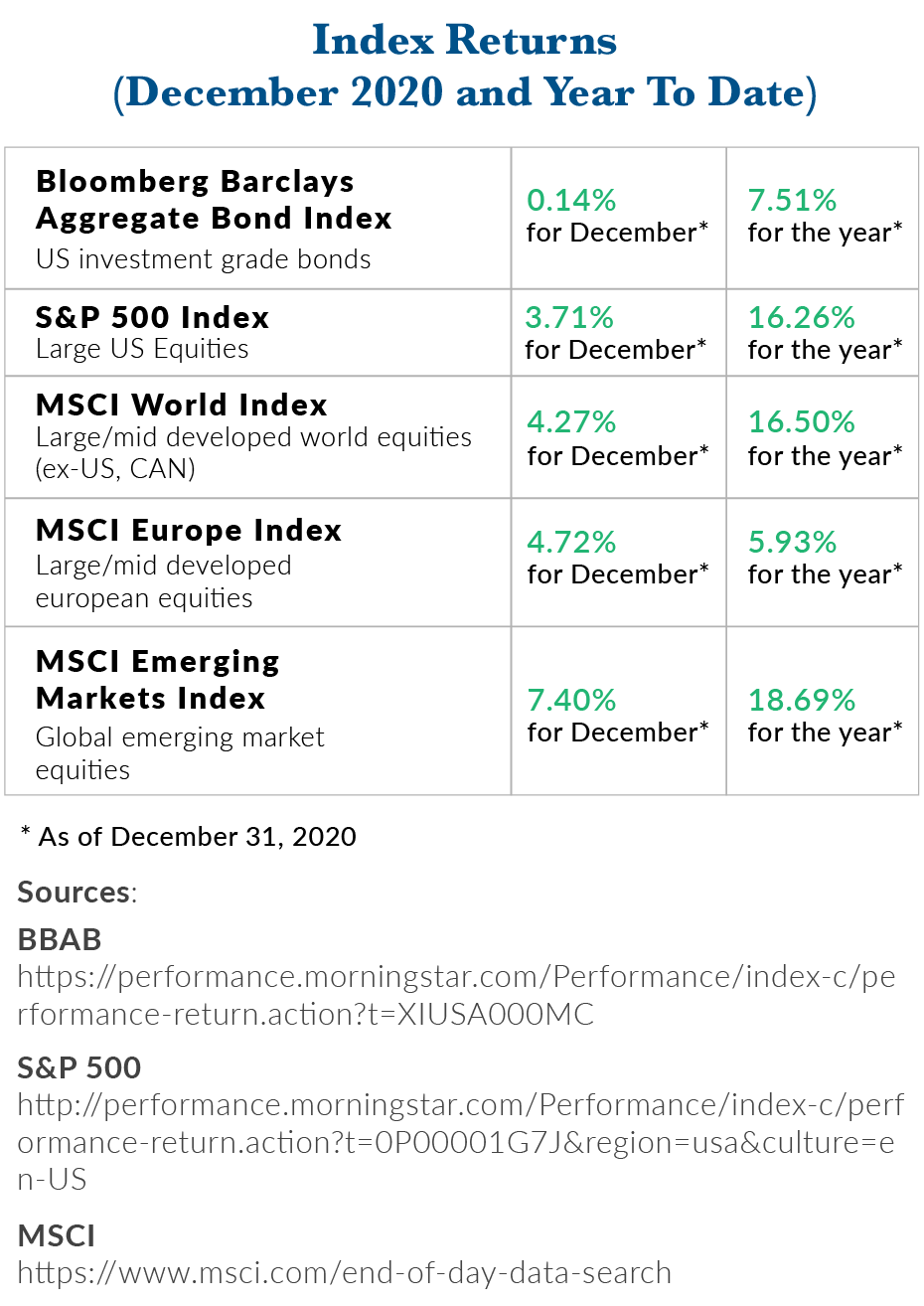

Shrugging off the pandemic, the economy, political turmoil, and a number of other events that would have been historic on their own, the S&P 500 rose an astonishing 16.26 percent in 2020.[4]

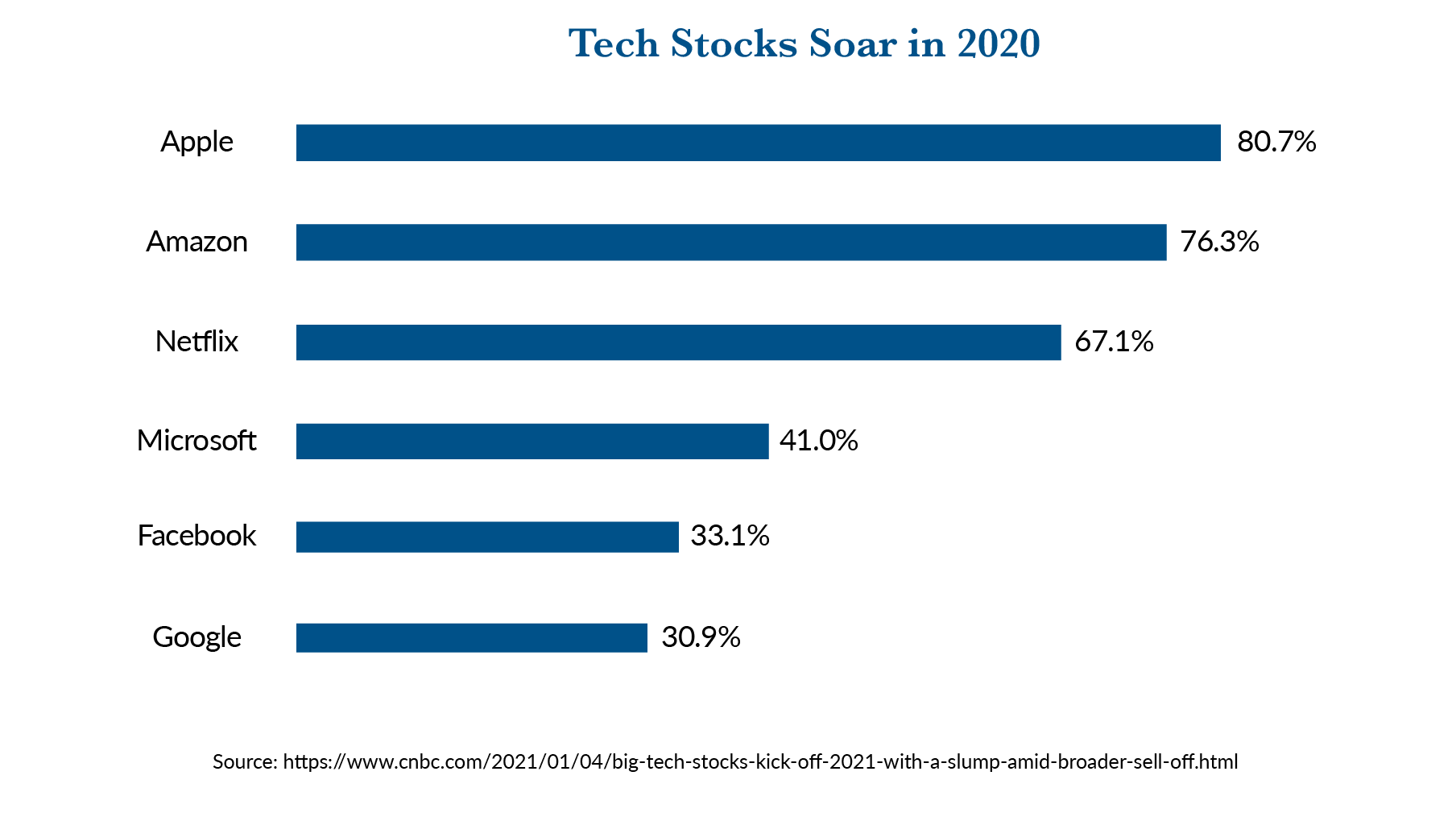

Notably, it was the largest technology stocks that contributed the most to these gains. The top five companies in the S&P 500 had an average 2020 return of almost 53 percent.[5] Unsurprisingly, technology was far and away the major driver of returns, with Apple, Amazon, and Netflix all posting gains above 60 percent for the year.[6]

It’s important to remember that, at this point, where tech goes the index will follow: any significant headwinds to tech stocks , including the threat of antitrust legislation, will likely be felt by equity investors more broadly.

While we do not expect any significant policy changes in the immediate term, any move by the Biden administration to break up or reduce the market power of major technology companies could have an impact on their market values, and thus on the S&P 500.

Do we need to worry about new COVID-19 strains?

Finally, another news item of note: new, more contagious strains of COVID-19 were discovered in the United Kingdom and South Africa.[7]

Early results indicate that the Pfizer/BioNTech vaccine offers protection against the British and South African strains, which could be good news for similar variants that arise.[8] However, in the meantime, the spread of these variants could prompt additional shutdowns to protect overburdened hospital systems.[9]

What this means for you

We include the news of new COVID-19 strains here because we believe it’s important for us to remember how much of this pandemic created uncertainty, and dramatic market volatility for us in 2020, both as individuals and as investors.

From our point of view, it is entirely possible that there could be more economic wobbles over the coming year given situations like these. Market pessimists point to high market valuations, an overly heated IPO market and the rage in crypto currencies and other non-traditional products like SPACs. Market optimists look towards a large supply of continuous fiscal and monetary stimulus to reignite the economy.

From our point of view, it is entirely possible that there could be more economic wobbles over the coming year given situations like these. Market pessimists point to high market valuations, an overly heated IPO market and the rage in crypto currencies and other non-traditional products like SPACs. Market optimists look towards a large supply of continuous fiscal and monetary stimulus to reignite the economy.

In either scenario, this isn’t cause for panic: rather, we continue to advocate for prudence, calm, and discipline.

There have been many challenges in the past year, and while many portfolios benefited, we cannot reasonably say that sharp market volatility is over and done with. Regardless of market sentiment, we believe that a disciplined, big picture viewpoint is best when it comes to wealth management, and we will continue to carry out your investment strategy with that philosophy in mind.

As always, if we can provide any additional support or answer any questions, we are here to do so. While many have recently experienced quarantines or lock-downs, please know that you are not alone—our team is always a phone call or “Zoom” away.

Securities are offered through Mid Atlantic Capital Corporation (“MACC”) a registered broker dealer, Member FINRA/SIPC.

Investment advice is offered through JSF Financial, LLC, which is not a subsidiary or control affiliate of MACC.

Confidentiality Note: This email communication including all attachments transmitted with it may contain confidential information intended solely for the use of the addressee. If the reader or recipient of this communication is not the intended recipient, or you believe that you have received this communication in error, please notify the sender immediately by return email or by telephone at (323) 866-0833 and PROMPTLY delete this email including all attachments without reading them or saving them in any manner. The unauthorized use, dissemination, distribution, or reproduction of this email, including attachments, is strictly prohibited and may be unlawful.

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of Mid Atlantic Capital Corporation (MACC). Neither JSF Financial LLC nor MACC gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase or sale of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or MACC as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Europe Index captures large and mid cap representation across 15 Developed Markets countries in Europe and covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 emerging markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

A special purpose acquisition company (SPAC) is a “blank check” shell corporation designed to take companies public without going through the traditional IPO process.[1][2] SPACs allow retail investors to invest in private equity type transactions, particularly leveraged buyouts. According to the U.S. Securities and Exchange Commission (SEC), “A SPAC is created specifically to pool funds in order to finance a merger or acquisition opportunity within a set timeframe. The opportunity usually has yet to be identified.

Sources:

[1] https://www.wsj.com/articles/u-s-recovery-will-cool-further-before-getting-vaccine-boost-wsj-survey-shows-11607612401?mod=article_inline

[2] https://www.bloomberg.com/graphics/covid-vaccine-tracker-global-distribution/?srnd=premium&sref=c4RUGNV1

[3] This section: https://www.wsj.com/articles/december-jobs-report-coronavirus-2020-11610080447?mod=hp_lead_pos1&mod=hp_lead_pos1

[4] Source: http://performance.morningstar.com/Performance/index-c/performance-return.action?t=0P00001G7J®ion=usa&culture=en-US

[5] BlackRock “Student of the Market,” January 2021.

[6] https://www.cnbc.com/2021/01/04/big-tech-stocks-kick-off-2021-with-a-slump-amid-broader-sell-off.html

[7] https://fortune.com/2021/01/08/will-the-vaccines-work-against-the-south-african-variant-of-covid-19-pfizer-moderna-oxford-astrazeneca-new-strain/

[8] https://www.marketwatch.com/story/pfizerbiontech-vaccine-appears-to-protect-against-u-k-and-south-african-covid-19-strains-study-finds-11610108542

[ix] https://fortune.com/2021/01/08/will-the-vaccines-work-against-the-south-african-variant-of-covid-19-pfizer-moderna-oxford-astrazeneca-new-strain/

Performance table sources:

BBAB: https://performance.morningstar.com/Performance/index-c/performance-return.action?t=XIUSA000MC

S&P 500: http://performance.morningstar.com/Performance/index-c/performance-return.action?t=0P00001G7J®ion=usa&culture=en-US

MSCI: https://www.msci.com/end-of-day-data-search