November 6 2020 Market Update

The Multitude of Highs and Lows

As of this writing, the election is on the verge of being called. However, despite the ongoing uncertainty, the markets have surged in recent days.

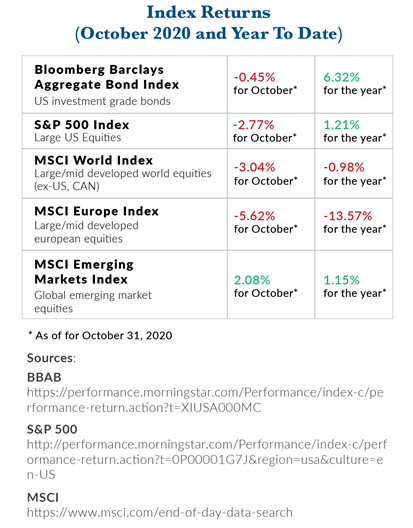

Taking a step back, the S&P 500 fell for a second straight month in October, paring back more of the year’s gains. Major contributors to the month’s volatility included dwindling prospects for a second round of fiscal stimulus, growing worry about rising COVID-19 cases, and of course the election.1

More detail on that and some implications for investors in the coming months can be found in this newsletter.

For more information about the potential longer-term impact of the election, we highly recommend reading our recent white paper.

For more information about the markets, economy, and our view of prospects for the rest of 2020, read on!

A Sharp Economic Rebound

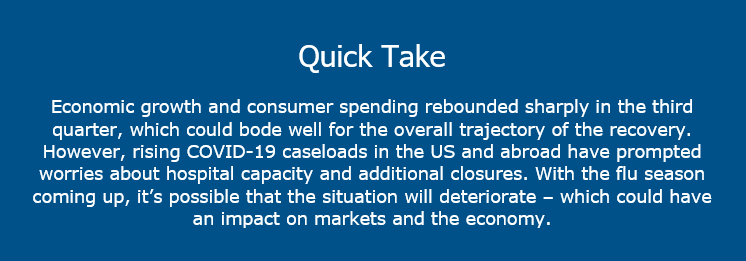

Following a record economic contraction in the second quarter, the U.S. economy rebounded. The third quarter’s annualized growth rate of 33.1% is the fastest ever, driven by a surge in business and consumer activity.2 Annualized rates infer what the growth rate would be if it lasted for a full year.

An important component of economic growth in the U.S. is consumer spending, and it looks like shoppers are coming back. After falling 6.9% in the first quarter, followed by 33.2% in the second quarter, personal consumption jumped 40.7% in the third quarter (please note: all rates are annualized).3 While this doesn’t get us back to the pre-pandemic baseline, it is a marked improvement.

One factor in consumer spending that hasn’t rebounded quite as quickly is employment. Almost half of the 22 million jobs lost to the pandemic have yet to be recovered, and the unemployment rate remains at an elevated 7.9%.4 Some researchers believe that when accounting for discouraged workers, or those who have given up on finding a job, the “true” unemployment rate might be over 10%.5

Closures Return as Virus Spreads

Since September, the number of new COVID-19 cases has been on the rise in the U.S.—and caseloads have accelerated in recent weeks. Daily new cases climbed above 80,000 in late October, marking the highest figures seen since the start of the pandemic.6 In the hard-hit Midwest, the spike in cases has started to put pressure on hospital systems and healthcare facilities.7 Capacity and staffing constraints are a particularly significant risk factor in light of the upcoming flu season.

In Europe, surging COVID-19 cases and deaths have pushed several countries to re-impose lockdown orders. This second wave of non-essential business closures sparked renewed concerns over the health of the global economy.8

These developments could be cause for concern, both for the global economy and markets. While progress is being made in vaccine development, the resurgence poses a risk to the economic recovery—especially if widespread closures must be re-imposed in order to contain the virus.

The Presidential Election

We continue to emphasize prudence in the ongoing uncertain environment.

On the political front, as of this writing the election result is on the verge of being called, but it is not yet 100% confirmed as votes continue to be counted. However, despite the uncertainty, the markets have surged in recent days. Investors have become comfortable with the notion of a potentially divided government whereby Republicans maintain control of the Senate.

At this point, the market has priced in a greater likelihood of a Biden victory.9 Meanwhile, the potential for a contested result appears more likely given President Trump’s legal actions in certain battleground states.

This may prolong the period of election uncertainty and prompt a degree of volatility.

In terms of policy, the prospects for a second stimulus package remain unknown. At this point, we believe that further economic stimulus is unlikely to be viable until late in the first quarter, or even the second quarter, of 2021. This could slow the pace of the recovery.

That said, recent comment from Senate Majority Leader Mitch McConnell hinted at the possibility of a stimulus deal by year-end.10

Heading Toward Year-End

All in all, despite the post-election surge, there is still potential for a bumpy road as we head into the final months of the fourth quarter. From COVID-19 cases and related closings to election uncertainty and the stimulus stalemate, we believe it’s possible that we’ll see additional market swings.

However, we do not believe that this is cause for alarm.

Time and time again, the markets have endured volatile conditions for a wide variety of reasons. The “animal spirits” of worried investors and those attempting to read the tea leaves of the future can run amok and may do so again over the coming months. In our view, it’s important not to join in.

Despite the pandemic-related challenges and polarized political environment, the economy looks to be on more stable footing than it was earlier in the year. Progress on the virus battlefront is continuing, and we hope there is an effective vaccine widely distributed by no later than next summer.

We will be closely monitoring the pandemic and election developments and their potential implications on the economy and markets. In the meantime, please don’t hesitate to reach out with your questions or concerns.

For an in-depth look at the outcome of the U.S. election and how investors should be thinking about the impact on the economic and investment landscape in 2021 and beyond, please join us on Monday, November 9 at Noon PST as we welcome Libby Cantrill, Head of Public Policy, PIMCO for a Zoom seminar. Click here to RSVP.

Securities are offered through Mid Atlantic Capital Corporation (“MACC”) a registered broker dealer, Member FINRA/SIPC.

Investment advice is offered through JSF Financial, LLC, which is not a subsidiary or control affiliate of MACC.

Confidentiality Note: This email communication including all attachments transmitted with it may contain confidential information intended solely for the use of the addressee. If the reader or recipient of this communication is not the intended recipient, or you believe that you have received this communication in error, please notify the sender immediately by return email or by telephone at (323) 866-0833 and PROMPTLY delete this email including all attachments without reading them or saving them in any manner. The unauthorized use, dissemination, distribution, or reproduction of this email, including attachments, is strictly prohibited and may be unlawful.

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of Mid Atlantic Capital Corporation (MACC). Neither JSF Financial LLC nor MACC gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase or sale of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or MACC as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Europe Index captures large and mid cap representation across 15 Developed Markets countries in Europe and covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 emerging markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

Sources:

1: https://www.cnbc.com/2020/10/29/stock-market-futures-open-to-close-news.html

3: https://apps.bea.gov/iTable/iTable.cfm?reqid=19&step=2#reqid=19&step=2&isuri=1&1921=survey

4: https://www.cnbc.com/2020/10/02/jobs-report-september-2020.html

5: https://www.ft.com/content/ec3d88dc-0dc1-4f6e-adf7-37e8f4316a22

7: https://www.politico.com/news/2020/10/16/pandemic-states-virus-rebound-429753

9: https://www.cnn.com/2020/11/04/tech/big-tech-joe-biden/index.html

Performance table sources:

BBAB: https://performance.morningstar.com/Performance/index-c/performance-return.action?t=XIUSA000MC