Back on the Seesaw

Quick Take: Equity markets bounced back from a two-month losing streak in response to 3rd quarter earnings and reports that the Fed could reduce interest rate hikes.[1]

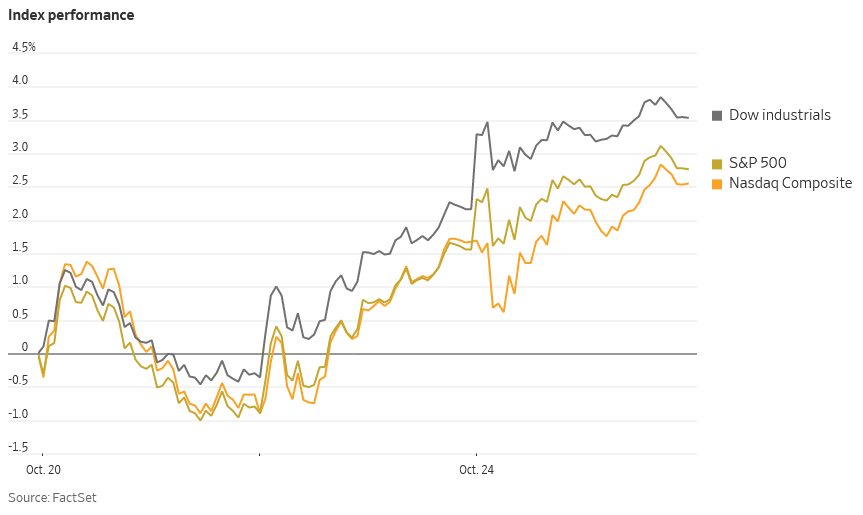

As the holiday season approaches, equity markets made a brief comeback as the S&P 500 index climbed 8% in October, the first monthly rise since July.[2] The Dow Jones Industrial index posted its best month since 1976.[3]

Even though major tech earnings disappointed investors, the tech-heavy Nasdaq also rose 3.9%.[4] Investors responded positively to earnings results and reports that Fed officials may consider shifting to smaller interest-rate hikes of 0.5% starting in December.[5]

Source: https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

Economy Watch

Notably for recession watchers, US gross domestic product (GDP) grew again in the 3rd quarter by 0.6%, after two quarters of decline. Key components of this broad measure of US activity showed signs of a slowdown, as the Fed tries to rein in inflation with restrictive rate hikes.[6]

Given the rebound in 3rd quarter GDP and a strong jobs market, we haven’t yet reached recession territory. However, 98% of CEOs surveyed by The Conference Board are preparing for a recession, and even the most bullish outlooks are assuming an upcoming recession.[7] Bloomberg economists expect a recession within the next year.

Rate hikes have driven US Treasury yields near their highest levels (lowest prices) of the past decade, with the 10-year Treasury yield trading above 4.2%.[8] These high yields could unearth opportunities in government bonds and even Treasury bills.

Wait and See

While markets tend to be forward-looking, the impact of interest rate hikes can have a considerable lag. After all, interest rate changes take time to filter through the economy. As borrowing costs rise and asset prices decline, consumer demand needs to slow to lower sales, so that companies can no longer raise prices.

Individuals and businesses may choose to slow the pace of borrowing and investing, but the lower demand that leads to businesses trimming their workforce is a multilevel process. Participants at the Federal Reserve’s (“the Fed”) September policy meeting noted that a significant portion of economic activity has still not had much of a response to higher interest rates.[9]

Source: https://www.wsj.com/articles/higher-interest-rates-can-take-a-long-time-to-bring-down-inflation-11666517405?mod=Searchresults_pos12&page=1

After months of rapid rate hikes, investors are hopeful that the Fed is nearing a pause or at least slowdown in interest rate hikes.

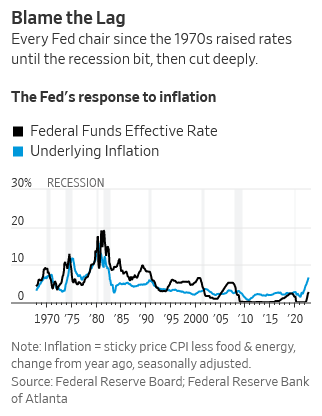

The market’s optimism over a potential turn in the rate hiking cycle has precedence. Looking back in history, every Fed chair since the 1970s has raised rates until a recession began, then pivoted to cut rates deeply.[10]

Continued high inflation and low unemployment could dash such hopes and pressure the Fed to press ahead with the hawkish policy to curtail inflation.

Earnings and a Bear Market Rally?

3rd quarter corporate earnings have been a mixed bag, with 35% of S&P 500 companies missing earnings.[11] Markets rallied as several corporate leaders expressed confidence in the strength of the consumer.[12]

Source: https://www.ft.com/content/af7de03e-8c68-41f5-ad79-1b82f4808482

While the US economy looks somewhat resilient, the reality is that we are seeing weaker growth and declining net profit margins in the S&P 500 companies. [13] Morgan Stanley Wealth Management Chief Investment Officer Lisa Shalett noted a disconnect between a lack of explicitly lower guidance during earnings calls and low levels of CEO confidence.[14] As a result, earnings estimates could still have room to fall.

Morgan Stanley strategist Mike Wilson, who until recently was a prominent stock market bear who predicted this year’s slump in equities, believes the October stock rally could have legs until the next earnings estimates pull back more meaningfully.[15] His view is that as markets transition to expect falling inflation and lower interest rates, stocks could grind higher in a bear market rally.[16] Of course, the timing of falling inflation and lower rates, along with the direction of the stock market, is still a major question mark.

Looking Ahead

Source: https://www.jpmorgan.com/wealth-management/wealth-partners/insights/midterm-elections-preview-potential-outcomes-and-market-implications

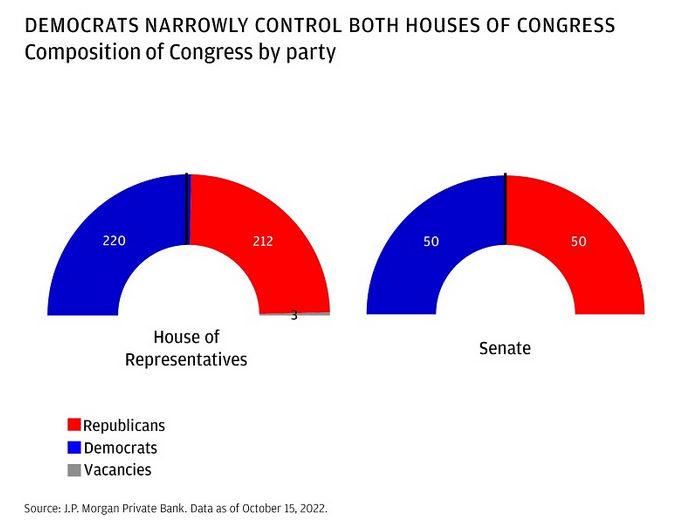

November brings the midterm elections, where analysts expect an uphill climb for Democrats. The consensus expectation for Democrats to lose seats in Congress could result in more gridlock, which historically tends to be positive for stocks.[17] Whether politics will have an impact against the tide of rising rates remains to be seen.

We’ll close out the year with one more Fed meeting in December. In November, the Fed, as widely expected, raised rates by 0.75% for the fourth consecutive time.[18] Investors parsed Fed minutes and Chairman Powell’s testimony, which indicates additional rate increases are on the horizon.

The October bounce back is another reminder of the unpredictability of markets and how quickly sentiment shifts. Most decisions based on short-term emotional views tend to be damaging to long-term performance. The bumpy ride underscores the benefits of a carefully pre-planned investing approach. Our experience through other “unprecedented times” has shown that long term investors are generally rewarded for staying the course.

Please reach out to schedule your year-end review or discuss any thoughts, concerns, or changes in objectives. We are blessed to live in a resilient country and look forward to honoring our great democracy by voting this week!

Your Friends at JSF

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

The Nasdaq Composite is a market-capitalization-weighted index consisting of all Nasdaq Stock Exchange listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds or debenture securities.

Treasury Bond- is a U.S. government debt security with a fixed interest rate and maturity between two and 10 years.

Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period. GDP is the most commonly used measure of economic activity.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

[1] https://www.cnbc.com/2022/10/30/stock-market-news-futures-open-to-close.html

[2] https://www.ft.com/content/af7de03e-8c68-41f5-ad79-1b82f4808482

[3] https://www.cnbc.com/2022/10/30/stock-market-news-futures-open-to-close.html

[4] https://www.ft.com/content/af7de03e-8c68-41f5-ad79-1b82f4808482

[5] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

[6] https://www.nytimes.com/2022/10/27/business/economy/us-economy-gdp.html

[7] https://www.morganstanley.com/ideas/q3-earnings-better-than-expected-how-long

[8] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-21-2022-11666349021

[9] https://www.wsj.com/articles/higher-interest-rates-can-take-a-long-time-to-bring-down-inflation-11666517405?mod=Searchresults_pos12&page=1

[10] https://www.wsj.com/articles/higher-interest-rates-can-take-a-long-time-to-bring-down-inflation-11666517405

[11] https://www.gsam.com/content/gsam/us/en/advisors/market-insights/market-strategy/global-market-monitor/2022/market_monitor_102822.html

[12] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

[13] https://www.wsj.com/articles/global-stocks-markets-dow-update-10-24-2022-11666608261?mod=Searchresults_pos11&page=1

[14] https://www.morganstanley.com/ideas/q3-earnings-better-than-expected-how-long

[15] https://news.yahoo.com/morgan-stanley-wilson-says-end-091001300.html

[16] https://www.bnnbloomberg.ca/morgan-stanley-s-wilson-says-bear-market-may-end-in-early-2023-1.1837567

[17] https://www.nytimes.com/2022/10/28/business/midterm-election-stock-market.html

[18] https://www.blackrock.com/us/individual/insights/blackrock-investment-institute/weekly-commentary