A Bruising First Half Performance: June 2022 Markets

Last month, we noted expectations from PIMCO Economist Allison Boxer of a rapid summer monetary tightening cycle with a focus on taming inflation.[1]  The story in June again revolved around fighting inflation: after headline inflation data beat expectations, markets sold off in anticipation of a faster rate hike from the Federal Reserve. The Federal Reserve followed up with a 0.75% rate hike, the largest increase in rates since 1994.[2]

The story in June again revolved around fighting inflation: after headline inflation data beat expectations, markets sold off in anticipation of a faster rate hike from the Federal Reserve. The Federal Reserve followed up with a 0.75% rate hike, the largest increase in rates since 1994.[2]

Rising inflation and interest rates have fueled a rout that’s lasted several months across most markets, sparing pretty much only commodities prices.[3]

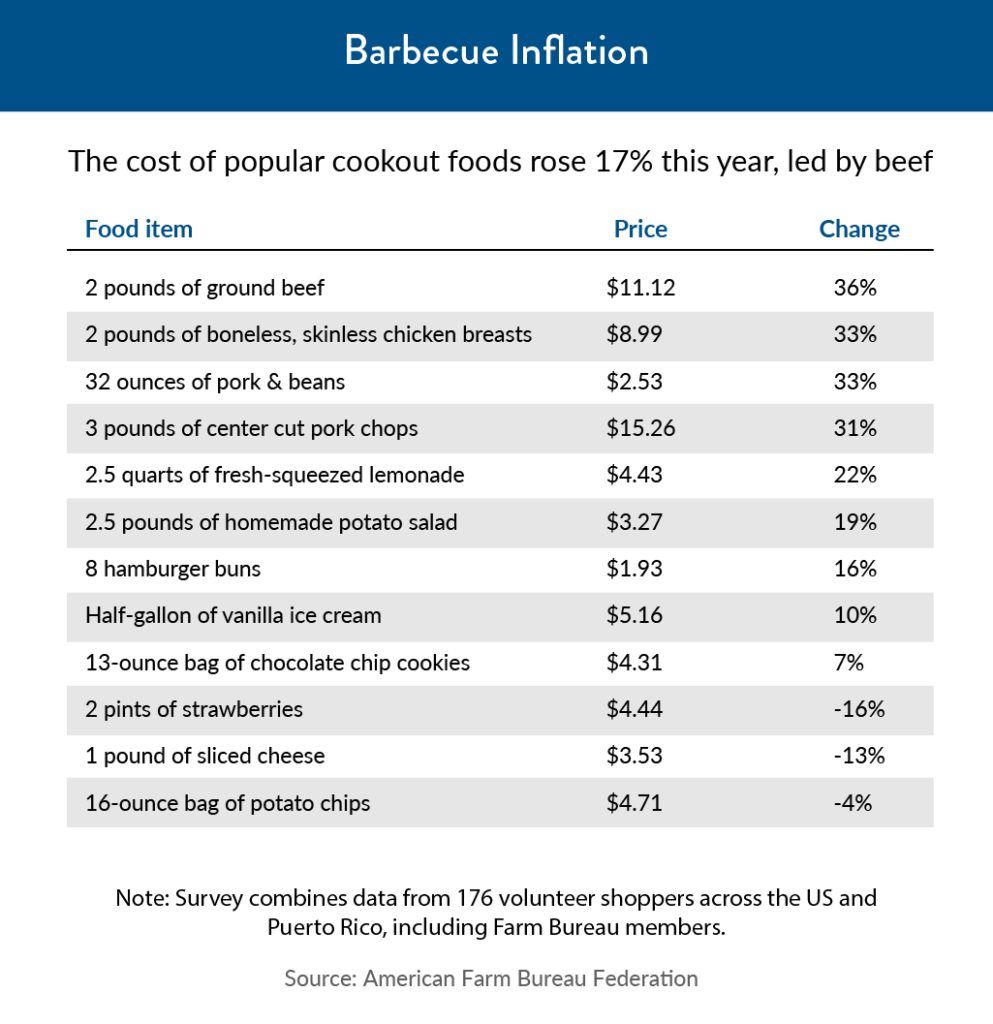

Inflation Hits Cookouts

Anyone barbequing over the Fourth of July weekend may have noticed a rapid increase in food prices. Popular barbecue foods like beef cost as much as 36% more this year compared to last year.[4] Chief economist of the Farm Bureau Roger Cryan pointed to Russia’s invasion of Ukraine as a major culprit in disrupting global supply chains, as costs for fuel, labor, and key farming inputs like fertilizer soared.[5]

Perhaps not surprisingly, shoppers were already pulling back on spending in May, and a measure of US consumer sentiment fell to an all-time low.[6] As demand cools, the hope is that prices will also start to come down. There are already signs that inflation might be tapering off: The personal consumption expenditures price index, which the Federal Reserve uses for its inflation target, rose less than expected in May.[7]

Risks of Tightening Financial Conditions

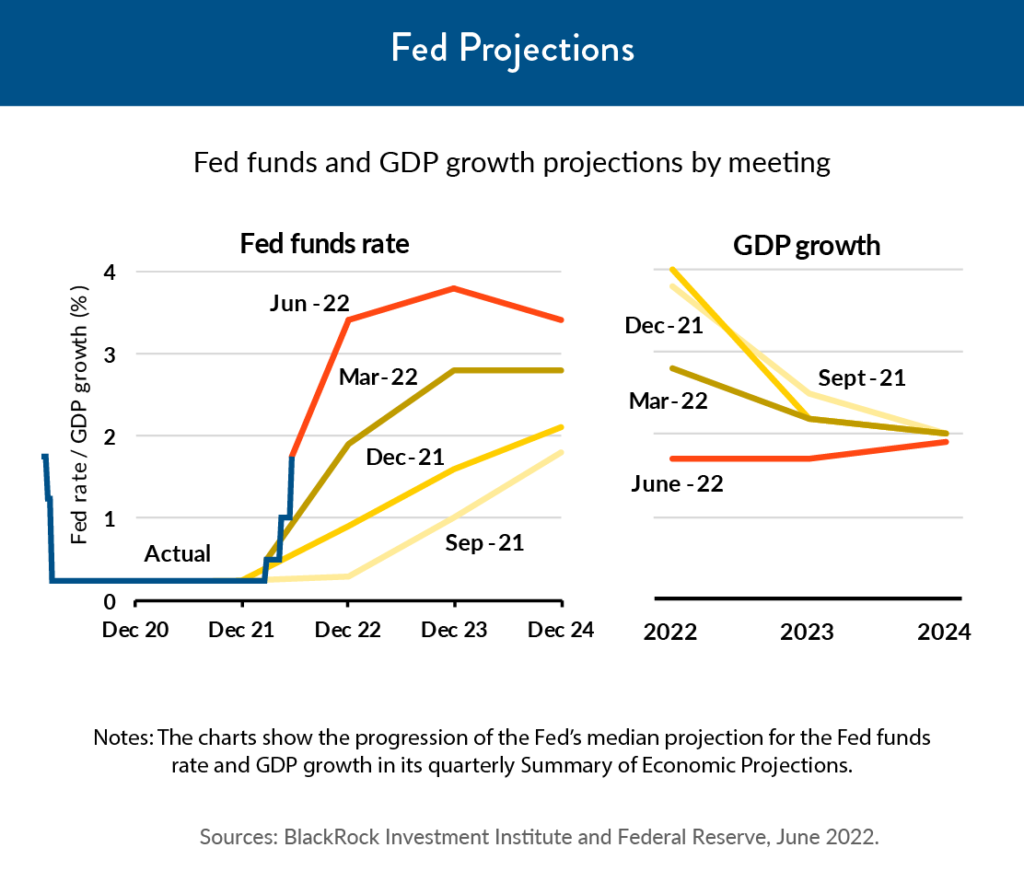

Investors have been closely following Fed policy as it executes the most aggressive pace of rate hikes since the 1980s.[8] During the June meeting, the Fed strengthened its language around inflation, saying it is “strongly committed to returning inflation to its 2% objective.” This is a shift from previous language, which expected “inflation to return to its 2% objective and the labor market to remain strong.”[9]

Fed projections now show that officials unanimously think the Fed funds rate needs to rise above neutral (the rate at which policy is neither supportive nor restrictive).[10] Markets were already pricing in rates above neutral, but now the Fed seems to have more consensus about a steeper path of rate hikes—even more so than at the May FOMC meeting.[11] Investors are now almost fully expecting a 0.75% rate hike in July.[12]

Not only is the Fed forcefully tackling inflation, but now they have conceded that the path to a soft landing has become “more challenging.”[13] After all, external factors like the Russia-Ukraine war and supply chain disruptions remain out of the Fed’s control.

That said, Fed officials believe that waiting to address high inflation would be a costly error, because it could require a more severe downturn later.[14]

It should be noted that the Fed anticipates inflation coming down to nearly 2% by 2024, with growth hardly dropping much below 2% and a modest rise in unemployment.[15] According to Michael Pond, inflation strategist at Barclays, the Fed’s outlook could work out due to easing supply chain constraints like falling freight rates and well-stocked retail inventories.[16] How this will play out remains to be seen.

Are we there yet?

Following the pain in the first half, the question is how much volatility remains in the stock and bond markets.

There are some possible indicators that we could be close to a market bottom, even if short-lived.[17] According to JPMorgan strategist Peng Cheng, retail investors have finally capitulated, exiting shares in June at the fastest rate in nearly two years.[18] When Bank of America surveyed its investors, it found that fund managers have larger than average cash positions, smaller than average equities positions, and a significantly high degree of pessimism about the economy.[19]

The best-case scenario would be a soft landing that brings down demand and inflation without severely impacting the economy. This month, we will receive a wealth of earnings and economic data, as well as another FOMC meeting which will impact the direction of the markets.

While we anticipate more volatility, we generally recommend a thoughtful, long-term, diversified approach, which lines up your assets with upcoming liabilities. Attempting to anticipate short-term market shifts is simply too risky. So often, markets turn when least expected. To that end, like always, we caution against making any emotional or rash decisions on investments and continue focusing on your diverse, long-term objectives.

If you’re feeling concerned, please do reach out to us to schedule a mid-year meeting: we would love to discuss your thoughts, questions, and concerns as they relate to markets and economics. We wish everyone a happy, healthy and sunshine-filled summer! Stay on the lookout for our ongoing webinar topics – since we offer them all virtually, we invite you to join us from land, sea, the comfort of home, or wherever your summer takes you!

View print version of this article.

The information expressed herein are those of JSF Financial, LLC, it does not necessarily reflect the views of NewEdge Securities, Inc. Neither JSF Financial LLC nor NewEdge Securities, Inc. gives tax or legal advice. All opinions are subject to change without notice. Neither the information provided, nor any opinion expressed constitutes a solicitation or recommendation for the purchase, sale or holding of any security. Investing involves risk, including possible loss of principal. Indexes are unmanaged and cannot be invested in directly.

Historical data shown represents past performance and does not guarantee comparable future results. The information and statistical data contained herein were obtained from sources believed to be reliable but in no way are guaranteed by JSF Financial, LLC or NewEdge Securities, Inc. as to accuracy or completeness. The information provided is not intended to be a complete analysis of every material fact respecting any strategy. The examples presented do not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy. Diversification does not ensure a profit or guarantee against loss. Carefully consider the investment objectives, risks, charges and expenses of the trades referenced in this material before investing.

Asset Allocation and Diversification do not guarantee a profit or protect against a loss.

The Bloomberg Barclays U.S. Aggregate Bond Index measures the investment-grade U.S. dollar-denominated, fixed-rate taxable bond market and includes Treasury securities, government-related and corporate securities, mortgage-backed securities, asset-backed securities and commercial mortgage-backed securities.

The S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

SPX, or the Standard & Poor’s 500 Index, is a stock index that is comprised of the 500 largest U.S. publicly traded companies by market capitalization, or the stock price multiplied by the number of shares it has outstanding.

The MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across 23 developed markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Europe Index captures large and mid-cap representation across 15 developed markets countries in Europe and covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 emerging markets countries and covers approximately 85% of the free float-adjusted market capitalization in each country.

By clicking on these links, you will leave our server, as they are located on another server. We have not independently verified the information available through this link. The link is provided to you as a matter of interest. Please click on the links below to leave and proceed to the selected site.

Sources:

[1] https://www.pimco.com/en-us/insights/blog/fed-outlook-expeditious-but-nimble/

[2] https://www.wsj.com/articles/fed-raises-rates-by-0-75-percentage-point-largest-increase-since-1994-11655316170

[3] https://www.wsj.com/articles/markets-head-toward-worst-start-to-a-year-in-decades-11656551051

[4] https://www.yahoo.com/now/inflation-hits-july-4-cookouts-181515381.html

[5] https://www.yahoo.com/now/inflation-hits-july-4-cookouts-181515381.html

[6] https://www.yahoo.com/now/inflation-hits-july-4-cookouts-181515381.html

[7] https://www.bloomberg.com/news/articles/2022-06-30/brutal-first-half-for-s-p-500-has-little-bearing-on-the-future

[8]https://www.wsj.com/articles/powell-says-pandemic-could-alter-inflation-dynamics-11656509259

[9] https://www.schwab.com/learn/story/fomc-meeting

[10] https://www.pimco.com/en-us/insights/blog/fed-battles-inflation-despite-the-costs

[11] https://www.pimco.com/en-us/insights/blog/fed-battles-inflation-despite-the-costs

[12] https://www.bloomberg.com/news/articles/2022-06-26/powell-s-path-to-2-inflation-needs-luck-or-failing-that-pain

[13] https://www.schwab.com/learn/story/fomc-meeting

[14] https://www.wsj.com/articles/powell-says-pandemic-could-alter-inflation-dynamics-11656509259

[15] https://www.bloomberg.com/news/articles/2022-06-26/powell-s-path-to-2-inflation-needs-luck-or-failing-that-pain

[16] https://www.bloomberg.com/news/articles/2022-06-26/powell-s-path-to-2-inflation-needs-luck-or-failing-that-pain

[17] https://www.bloomberg.com/news/articles/2022-06-23/jpmorgan-sees-capitulation-in-retail-crowd-bailing-on-stocks

[18] https://www.bloomberg.com/news/articles/2022-06-23/jpmorgan-sees-capitulation-in-retail-crowd-bailing-on-stocks

[19] https://www.wsj.com/articles/markets-head-toward-worst-start-to-a-year-in-decades-11656551051

Performance table sources: